")

- Banking that is done through the digital platform without any paperwork is referred to as digital banking

- Digital banking means the availability of banking services online

With the Indian Government’s vision of a cashless economy and rapid development in improving internet availability throughout the nation, the country recorded over 48.6 billion real-time payment transactions in 2021 (the highest in the world) exceeding China by 162 %.

Digital Banking Meaning

Digital Banking is the automation of traditional banking services. Digital banking enables a bank’s customers to access banking products and services via an electronic/online platform. Digital banking means digitizing all of the banking operations and substituting the bank’s physical presence with an everlasting online presence, eliminating a consumer’s need to visit a branch.

Benefits of Digital Banking

Advancing to a more technologically sophisticated way of doing things, it goes without saying that the benefits long outweigh the costs. Similarly, digital banking as a technological by-product aims to make life easier for the customers of a bank. Digital banking has the following benefits:

- Digital banking enables consumers to perform banking functions from the comfort of their homes, be it an elderly person who is tired of waiting in lines or a working-class professional who is caught up with work, or a regular person who does not want to visit the bank’s branch to run a single errand. It also offers convenience.

- Elaborating on the convenience offered, digital banking lets a user carry out banking work around the clock, with 24*7 availability of access to banking functions.

- One of the biggest drawbacks of traditional banking was the overly placed importance on paper. Banking has become paperless with the development of digital banking as a service. A user can log into their account at any point in time to monitor records.

- Digital banking allows a user to set up automatic payments for regular utility bills such as electricity, gas, phone, and credit cards. The customer no longer has to make a conscious effort of remembering the due dates. The customer can opt for alerts on upcoming payments and outstanding dues.

- Online shopping has become a cakewalk with payment channels becoming well-integrated with online shopping portals. Internet banking has significantly contributed to online payments.

- Digital banking extending services to remote areas is seemingly a step toward holistic development. With smartphones at affordable prices and internet access in remote areas, the rural population can make the most out of digital banking services.

- Digital banking-enabled fund transfers reduce the risk of counterfeit currency.

- With the help of digital banking, a user can report and block misplaced credit cards at the click of a button. This benefit greatly strengthens the privacy and security available to a bank’s customers.

- By promoting a cashless society, digital banking restricts the circulation of black money as the Government can keep a track of fund movements. In the long run, digital banking is expected to lower the minting demands of a currency.

Read more about how Digital banking and Online shopping is helping India here.

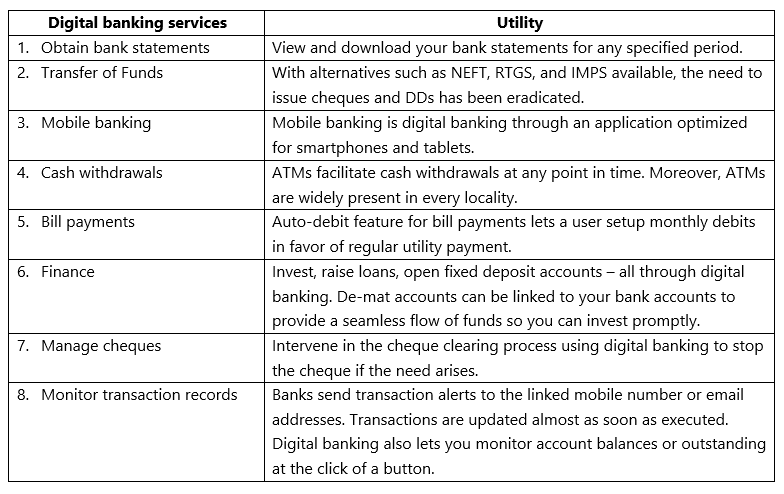

Digital Banking products

If an individual has access to a stable internet connection and an internet-enabled smart device, digital banking has a lot to offer.

Digital Product services

Source: Tavaga Research

Types of Digital banking payments

- Banking cards: Cards are not only used to withdraw cash but also enable other forms of digital payment. Cards can be used for online transactions and on Point of Sale (PoS) machines. Prepaid cards can also be issued by banks; such cards are not linked to the bank account but function through the money loaded onto them.

- Unstructured Supplementary Service Data (USSD): By dialling the number *99#, mobile transactions can be carried out without an application and internet connection. The number holds nationwide applicability and promotes greater financial inclusion on the ground level. The service lets the caller surf through an interactive voice menu and chooses the desired option on the mobile screen. The only catch is the mobile number of the caller should be the one linked to the particular bank account.

- Aadhaar Enabled Payment System (AEPS): AEPS lets the client initiate banking instructions following the successful verification of the Aadhaar number.

- Unified Payments Interface (UPI): UPI is the trending form of digital banking presently. UPI makes use of a virtual payment address (VPA) so the user can transfer funds without entering bank account details or an IFSC code. Another striking feature of UPI is that the applications let you consolidate all your bank accounts in one place. Funds can be transferred and received around the clock with no time restrictions. UPI-based apps in India are BHIM, PhonePe, and Google Pay. BHIM application, in addition to the transfer of funds to other virtual addresses and bank accounts, also lets the user transfer funds to another Aadhaar number. Click here to know about RBI’s digital payment initiative announced last September. More importantly, UPI-based payments are free of cost. Want to know more about UPI-linked credit cards, Click here.

- Mobile Wallets: Mobile wallets have eliminated the need to remember four-digit card pins or enter CVV details or carry loose cash. Mobile wallets store bank account and card credentials to easily add funds to the wallet and make payments to other merchants with similar applications. Popular mobile wallets are Paytm, Freecharge, MobiKwik, etc. Mobile wallets, however, generally have a limit on how much can be deposited in the wallet. A small fee may also be charged on depositing the funds from the mobile wallet back into the bank account.

- PoS terminals: Typically, PoS machines are portable devices that read a card to authorize and complete the payment. Supermarkets and gas stations opt for this method of payment. However, with digital banking thriving, PoS terminals have evolved into more than physical PoS devices. Virtual and Mobile PoS terminals have surfaced, which make use of the mobile phone’s NFC feature and web-based applications to initiate payment.

- Internet and Mobile Banking: Commonly known as e-banking, internet banking refers to obtaining certain banking services over the Internet, such as fund transfers, and opening and closing accounts. Internet banking is a subset of digital banking because Internet banking is only limited to core functions. Similarly, mobile banking is availing banking services through mobile-based applications. There is also a rise in banks without physical branches fuelled by mobile banking. Click here to learn more about Neo Banks.

Difference between Digital Banking and Online banking

More often than not, the terms digital banking and online banking are used interchangeably. However, there exists a fine line between the meaning of the terms.

Online Banking deals with everyday essentials, such as checking balances, reviewing transactions, and transferring funds. This is the core operation of the bank, which is shifted to an online presence with the help of online banking. Online banking is a means to an end.

However, digital banking is an end in itself. Digital banking is aimed at digitizing all the operations of the bank, core, or non-core. Starting from onboarding clients to servicing the accounts to the closure of accounts is digital banking’s primary objective. Digital banking’s agenda is to make the physical presence of a bank’s branch redundant for its customers so that the customers can handle all banking operations from their place of convenience. Therefore, online banking is a subset of the master set, of digital banking.

Disadvantages of Digital Banking?

Is digital banking safe? Contrary to the popular opinion that digital banking poses security concerns, most readers will be surprised to know that digital banking is safer as compared to traditional branch banking. While digital banking forums are prone to vulnerabilities and hacks such as phishing, pharming, identity theft, and keylogging, banking institutions are investing a lot in their security systems. Security is at the forefront when considering a service such as digital banking. If security were to be compromised, banks would lose a crucial selling factor, and more so than risking user data and resources, banking institutions cannot afford negative publicity.

In a hypothetical scenario where banks do lose your money to a hacker, you will be entitled to receive the due amount of your bank balance for the sole reason that your money is protected. Therefore, to avoid massive public liability and bad publicity, banks are bound to invest heavily in reinforcing the security of digital banking platforms.

However, a digital banking user must do their part by following certain practices that act as a safeguard:

- Follow the prompts to change your passwords regularly and keep your passwords confidential.

- Avoid using public networks and devices to access digital banking – if you must use a public device, remember to clear cache and browsing data. It is good practice to not allow the browser to save your username and password for bank details.

- Banks never ask for confidential information so refrain from sharing it with anyone who asks for it.

- Anti-virus-protected systems offer another layer of security to your systems.

- The URL address MUST begin with ‘https’, or a padlock must appear next to the website address. The padlock is a security certificate. The address bar turns green when the site is secured with an SSL certificate, which is an additional validation for the security of the website. Therefore, use the bank’s URL and refrain from clicking on other links. Banks generally use minimum SSL/128-bit encryption.

- Lastly, disconnect from the internet when the system is left idle.

Digital Banking in India

When did Digital Banking start in India?

In India, digital banking started taking shape in the late 1990s with ICICI Bank being the first one to bring the service to their retail clients. Digital banking became mainstream only in 1999 as internet charges were reduced and there was increased awareness and trust concerning the internet. It was only after the internet further developed and the costs came down, banks started serving a broader basket of products online.

Which is the best digital bank?

There is a list of companies providing offering the opening of a digital savings bank account. A digital savings account is no different than a basic savings bank account in that a digital savings bank account also allows a user to avail full banking facilities without any constraints of maintaining a minimum balance. The user is also entitled to a virtual debit card convertible to a physical debit card. The banks also offer net banking services through their portals like HDFC net banking or ICICI net banking etc.

Some of the best zero-balance digital savings bank account in India:

- Axis Bank ASAP

- Digisavings – DBS

- Kotak 811

- Pockets and Insta Save FC Account – ICICI Bank

- Indus Online Savings Account – IndusInd

All the above bank products offer differential services based on the accounts chosen. Some of the services can be attained by logging onto their website whereas others require an application. All accounts are enabled for fund transfers in the form of IMPS, NEFT, and UPI. Pockets by ICICI also offer the facility of NFC payments. Each account may offer more variants with differing levels of service and charges.

How can I do Digital Banking?

For any individual to do digital banking in India, you need to first open a checking or savings account with the bank. This can be done by visiting the branch in person, or by using the online account opening options on bank websites where you just have to upload a few documents from the comfort of your home.

Once you have an account ready with a bank, most banks will provide you with your digital banking credentials which can be used to do seamless transactions 24*7. If you do not receive your credentials in the welcome kit, you can always contact your bank to provide net banking free of cost.

To create a digital banking account in India, the individual must:

- Be over 18 years of age

- Have both PAN and Aadhaar Card

- Complete KYC, i.e., paper-based verification of details within twelve months of opening the digital bank account. Failure to comply with the norm will take away the individual’s right to open a digital bank account with the same Aadhaar and PAN in the future

As an improvisation to physical verification for KYC, the market regulator may allow video-based verification in the future to improve the process from a digital point of view.

Future of Digital Banking

As per a Deloitte research report on must-haves for a fully digital bank, each bank striving to become fully digital require the following as the key drivers for their success

- Option to order currency

- Customizable standing options

- Accounts linked to tax exemptions status

- Card blocking feature

- Innovation toward safety vaults

- Integration with stock market investment channels

- Financial management analytics

- Enable grouping of accounts of different banks

- Easily accessible assistance

A full-fledged replacement of physical branch banking with digital banking right now seems like a far-fetched dream. Digital banking comes in handy for recurring banking essential functions. However, customers prefer human interaction for more important and irregular decisions, such as while taking a loan or negotiating the terms of the loan.

For further Read: Check out our article on mobile wallets by clicking here.

3 comments

[…] options for interest due. Some banks offer a mobile-based application to operate the account with digital banking […]

[…] a part of the Digital India initiative, the Govt. mandated an open API policy, known as India Stack, giving third-party providers access […]

[…] which saw banks increase automation with better prospects of a total pledge cashless society. With digital banking, customers save more time and paperwork surrounding conventional banking while banks cut costs on […]