An overview of the banking sector for the last quarter of FY21 and expectations beyond.

Introduction –

The total banking assets of India according to various government surveys is approximately $2.33 trillion growing at a CAGR of 7% (approximately) from FY 14-19. The banking sector is growing at a skyrocketing rate and numbers are a concrete indicator that there is looking back. As a matter of fact, roughly 179 bank accounts are opened in the country every minute.

The pandemic has been a catalyst for the boom of the online banking and transaction side of the whole banking industry. The increasing number of users and building trust on the internet has been reflected in the corrections and growth of the banking sector.

This piece focuses on investor action associated with the banking shares for the future. Additionally, it highlights the recent and upcoming performance of the major players in the sector.

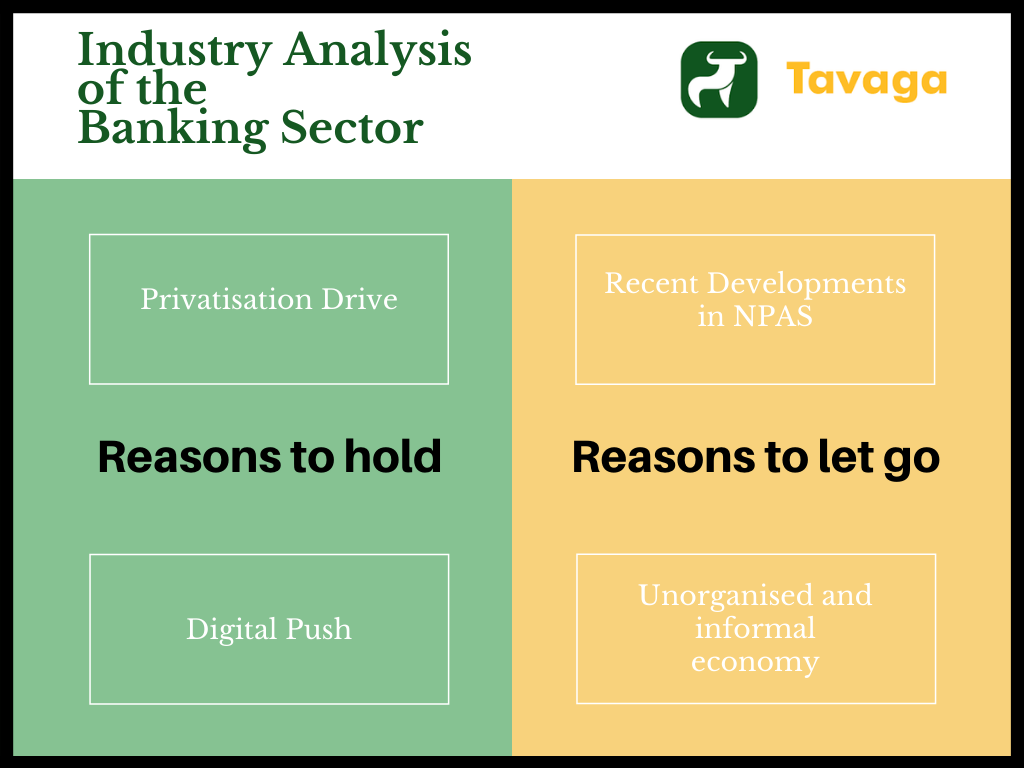

Top reasons to hold banking stocks-

Privatisation drive

Finance Minister Nirmala Sitharaman in her budget speech of FY 21 announced the privatisation of two public sector banks. The government holds stakes in the Punjab and Sindh Bank, Bank of Maharashtra, UCO Bank and IDBI and now wishes to sell them to fund other infrastructure projects.

One of the crucial reasons for this push for privatisation is the crunch that the government is facing due to an unexpected decrease in tax collection and an increase in NPAs. There is also a governmental debate and discussion around which entities and how much stake to sell-off. There is also a memo circulating to restructure the banks before the handover.

The previous privatisation drives have been proven extremely successful to not only fund the government but also for the industry as well. Better management and lesser governmental interference will be a positive indicator for the banking sector in near future.

Digital Push

As a part of the Digital India initiative, the Govt. mandated an open API policy, known as India Stack, giving third-party providers access to the proprietary software for five key programs: Aadhaar (the Government’s biometric identity database), e–KYC, e–signing, privacy-protected data sharing and the UPI.

Digital integration will bring a paradigm shift in the banking industry. Indian banks despite the grave economic and credit crisis have embraced this challenge as an opportunity with help of various fintech platforms. The global pandemic highlighted the importance of maintaining a digital footprint without any physical infrastructure. Thus, digital banking is the future of banking.

With the digital push and technological advancements, banks can move to an asset-light model, and invest in creating a seamless digital experience for their customers. RBI has also announced waving off charges on NEFT and RTGS. Conclusively moving digital and making investments in a sustainable manner highlight a positive outlook for the industry.

Top reasons to let go of banking stocks-

Recent developments around NPAs-

The Reserve Bank of India (RBI) defines NPA as “ An asset makes non-performing when it stops to generate income for the bank”. The beginning of this century witnessed an unprecedented increase in commercial or non-food credit. The Indian companies were borrowing aggressively to capitalise on the growth opportunities. However, all this investment went into infrastructure and related areas and the financial crash of 2008-09 lead to a decrease in profits and increased regulations. To top it all various credit rating agencies and lending institutions relaxed their lending requirements and compliances.

To curb the increased lending and debts the administration decided to re-examine the provisions of the Recovery of Debt Due to Banks and Financial Institutions Act, 1993, make the cash reserve ratio or (CRR) attractive, establish a credit information bureau and likes. The most important development was the Supreme Court lifting the blanket ban on NPA classification.

The performance of the banking sector had improved in FY20 with several PSU banks reporting high growth along with high NPAs. According to multiple stress tests performed by the RBI Indian bank’s gross bad bank loans could reach their highest level in nearly two decades. Banks are facing a lot of trouble due to various reasons including the unexpected pandemic and would need a lot of stimulus than mergers to sustain profitability.

Unorganised and informal economy –

The unorganised sector of the money market is flocked with local banks, lenders, traders and commission agents. The unorganized sector deals with agents who combine money lending with other activities.

The unorganised sector as one would guess is largely outside the purview of the Central Bank or any regulatory body. The Indian money market is dominated by the unorganized sector and informal economy. The rural area is clouded with rustic cooperative societies controlled by the money lenders who charge brutal interest rates. This informal segment of the economy escapes the tax net and adds to the accumulation of black money.

With the lawlessness in the market and limited population having access to a developed money market, the banking industry may have to work a little harder to penetrate its roots in the real Indian economy.

It is raining results –

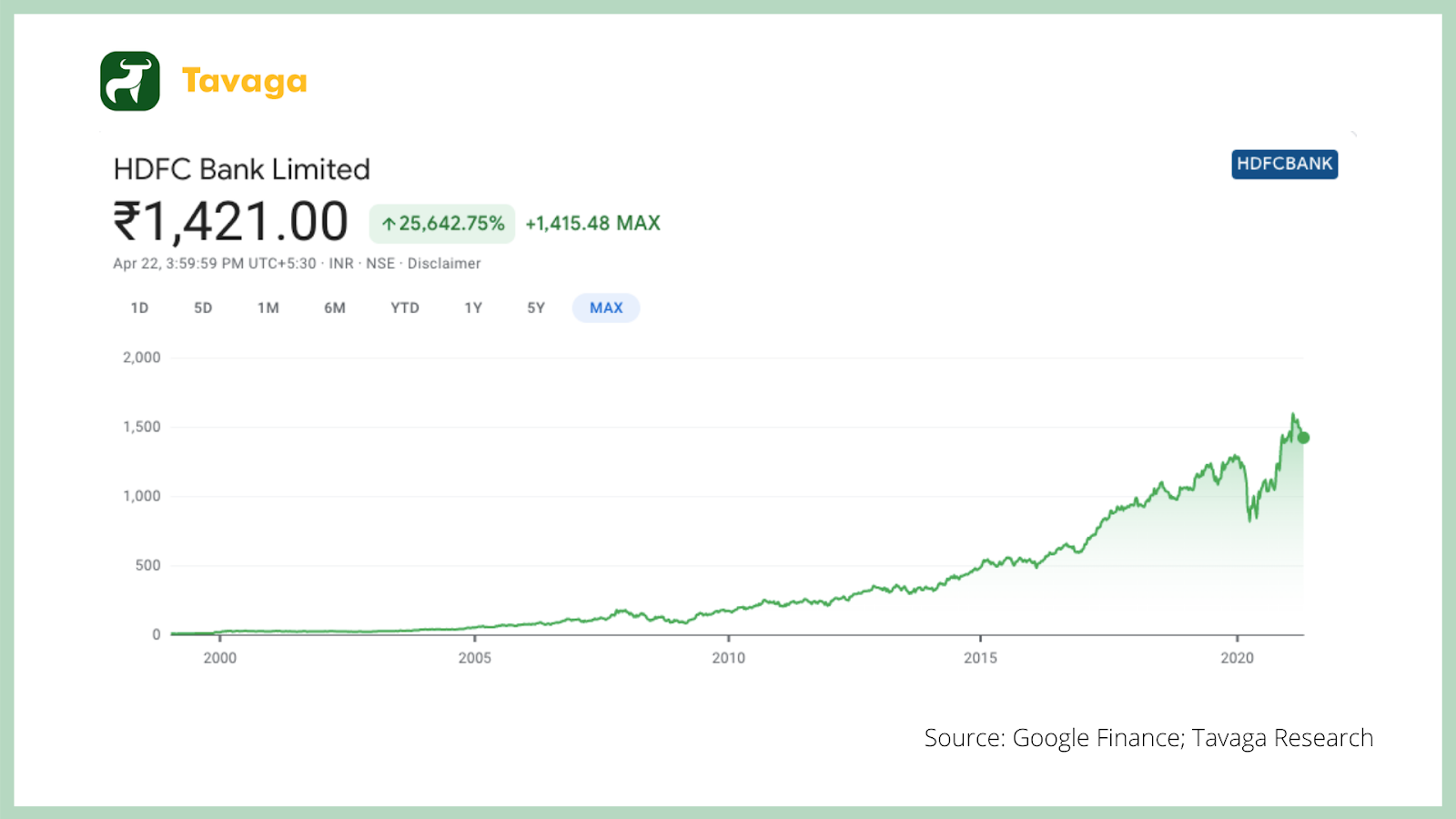

HDFC Bank –

India’s largest money lender reported a net profit of Rs. 8,186 CRS. for the March quarter which is 8.17% year-on-year. The net revenue stood at Rs. 24,713 CRS.

The bank reported steady growth in profits as the other income rose while bad loans and NPAs remained in check. The bank remains a strong franchise with solid cross cycle asset quality and superior return ratios.

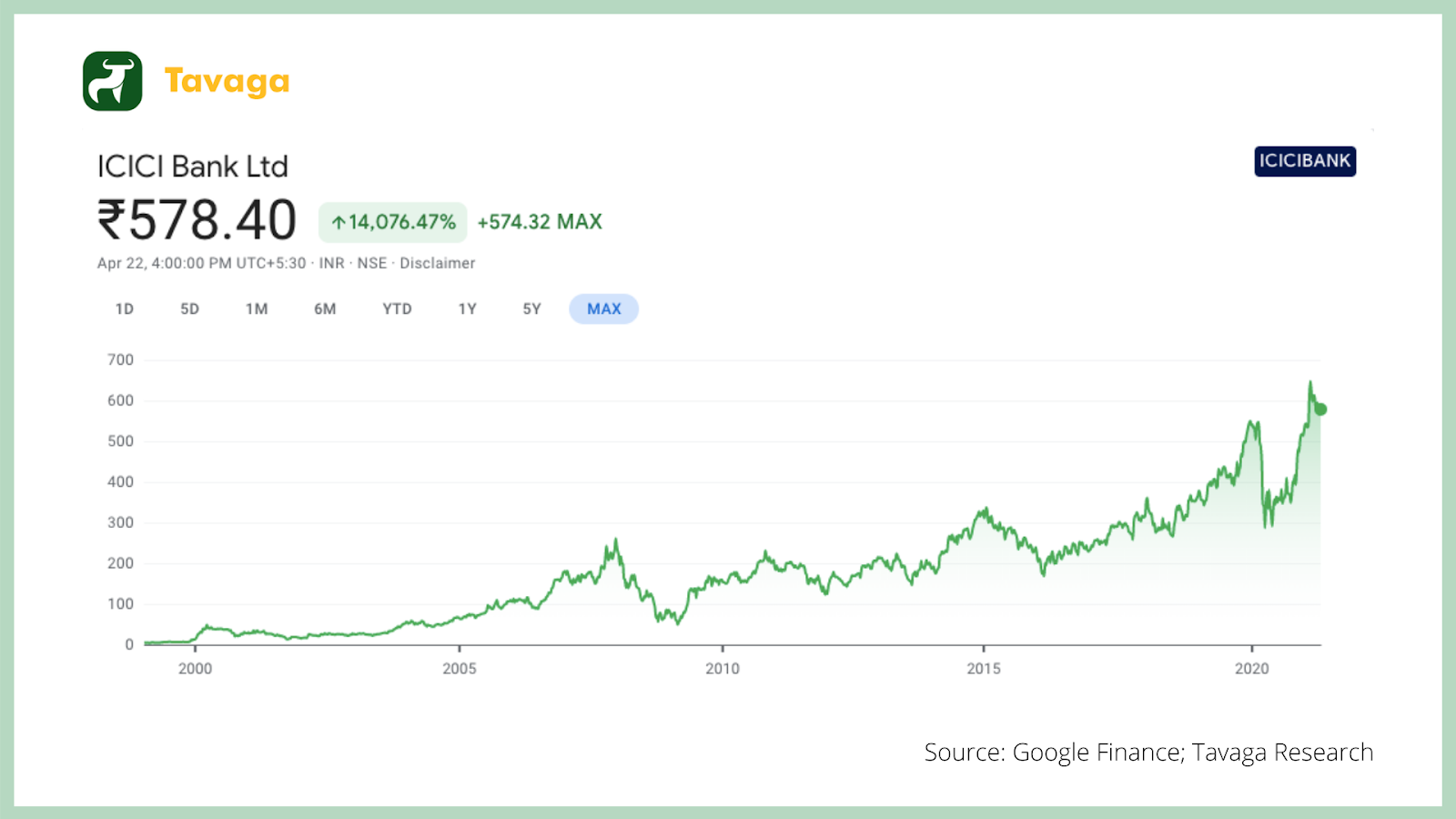

ICICI Bank

Industrial Credit and Investment Corporation of India or ICICI Bank was formed in 1955 as an initiative of the World Bank and the Government of India. The profit after tax of the bank is estimated to be approximately Rs. 4,940 CRS. The Net Interest Incomes is estimated to stand at Rs. 10,136 CRS.

The bank has made pandemic related provisions and there is an additional fund in the NPA pool. However, the bank has seen steady growth in loans and deposits.

Bandhan Bank

Bandhan Bank is a fairly newer entrant in the micro-lending sector. The Bank has recently changed its policy to one loan per person is adding to its efficient results. The profit after tax of the company is estimated to be at Rs 696 CRS. and the NII is projected to at Rs. 2325 CRS.

The micro-lender is facing relatively lower competition and has a longstanding reputation in East and North East India. In numbers, the bank has announced a collection efficiently of 95% for microfinance loans and 96%overall.

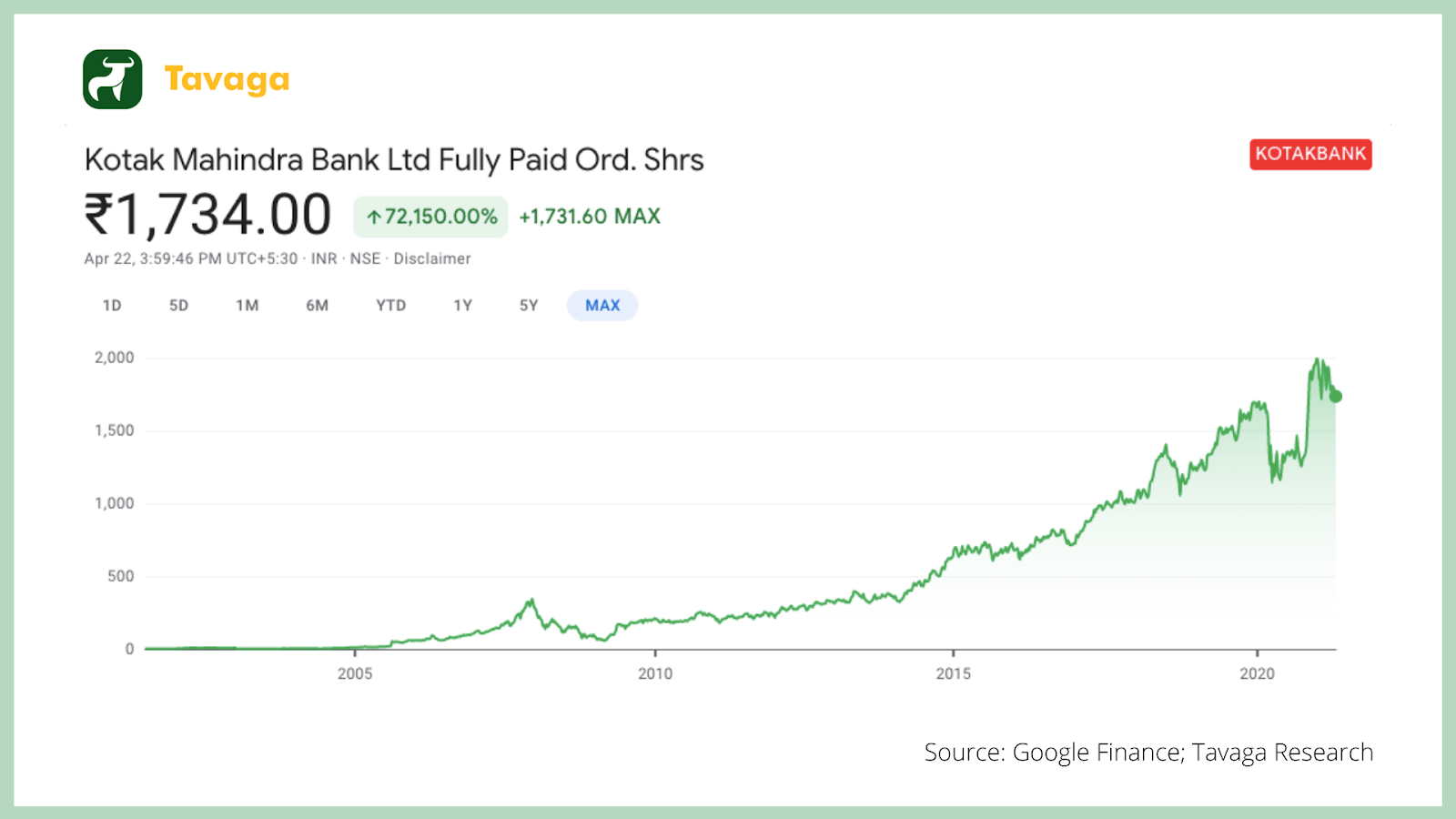

Kotak Bank

Since the inception of Kotak Mahindra Finance Ltd. in 1985, Kotak Mahindra Bank has become India’s most trusted financial lender. It is India’s first NBFC to be converted to a Commercial bank. The NIIs are expected to stand at Rs. 3,920 CRS. while the profit after tax is projected to be at Rs. 2,216 CRS.

With the plans of expansions and technological alternatives clubbed with decent financial health the future of the bank looks buoyant.

A better and easy way to put your money at work-

Bank ETFs or Bank Exchange Traded Funds offer investors vast exposure to the banking and financial sector of the economy. Bank ETFs are an easy way out for investors to share in the profits of the bank by investing in a basket of banks and financial service companies without being actively involved in the market.

A few of the best performing Bank ETFs for the Indian market are as follows* –

- Nippon India ETF Nifty BeEs

- SBI ETF Banking

- Edelweiss ETF – Nifty Bank

A few points before you make up your mind –

With all things said and done, it is extremely important to understand that as investors it is nearly impossible and rather dubious. To highlight that the banking sector will reach new highs or plummet in the near future is inconclusive and misleading.

PSU banks and overall government-run industries, in general, are usually considered to be strong companies to hold ownership in but there is no guarantee that they will perform well given the uncertain nature of the market.

Diversification of the portfolio or quick health check-up for an investors’ portfolio is highly recommended for hedging against inflation and market volatility. To not put all your eggs in one basket is usually a better strategy.

For more information on portfolio diversification and check up feel free to contact – +91 96190 39356

Tavaga is everything you need to start saving for your goals, stay on track, and achieve them in time.

Download Now:

* Team Tavaga has no direct or indirect monetary association with any of the ETFs or financial investment tool mentioned in the list.

Disclaimer – The above writeup is solely for the purpose of educating investors. It should not be considered as any direct or indirect advice on buying or selling of certain stocks mentioned above.