")

Indians have a long-standing love affair with Public Provident Fund (PPF). This savings scheme launched by the Government of India in 1968 encouraged long-term savings among the masses. Over the years, PPF gained immense popularity among Indian investors due to its attractive interest rates, tax benefits, and the guarantee of a risk-free return.

PPF is sovereign backed making PPF investments entirely secure. Moreover, the interest rate offered on PPF is fixed and reviewed every quarter thus removing any risk of market fluctuations. This has made PPF an ideal investment option for risk-averse investors.

PPF have often found favour among Indians looking for retirement investments because of its long-term horizon. The maturity period of PPF is 15 years, which can be extended in blocks of 5 years. This means that investors can continue to invest in PPF for a long time and build a substantial corpus for their retirement.

Anyone irrespective of their age can open a PPF in any bank or post office, thus making it accessible to all Indians. In short, PPFs have been a darling and the go-to investment option for all our fathers and uncles for ages.

But this love has unfortunately become one-sided. Once heavily promoted by the government, PPFs seem to have lost their importance in favour of other saving schemes. This was evident in a recent announcement by the government.

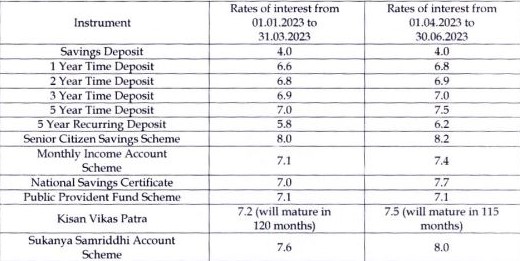

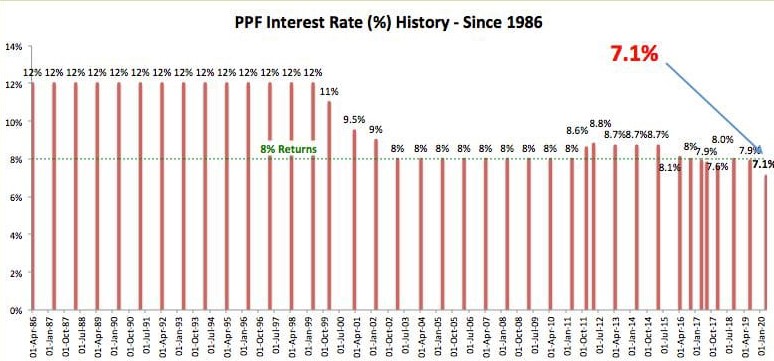

The government increased rates for “almost all” small savings schemes for April- June 2023, except Public Provident Funds (PPF). The rates for all other instruments have seen a hike of 0.10-0.70%, while PPF interest rates remained unchanged at 7.1%. Interest rates on PPF have infact not changed for last 3 years.

What determines the rate of interest on PPFs?

The interest rate for the PPF and other saving schemes is set every quarter based on various economic factors. The Shyamala Gopinath Committee set up by RBI in 2011 had suggested a formula for setting interest rates on small savings schemes in India, including PPF and National Savings Certificate (NSC), and others. The committe recommended making the returns of small saving schemes market-linked and benchmarked to those of government securities (G-secs) of similar maturity periods with a positive mark-up. For PPF the markup was 25 basis points (bps), for Senior Citizen’s Savings Scheme (SCSS) – it was 100 bps and for National Savings Certificate (NSC) was 50 bps. So if a 10-year G-sec yields are 8%, then the rate of interest for PPF would be 8.25%, i.e. 8% plus a mark up of 25 basis points.

Due to political opposition against this formula, the government decided not to implement it. Instead, the government continues to set the interest rates based on its own methodology, which takes into account several factors, including the prevailing market conditions, inflation rate, and fiscal deficit.

The interest rate for the PPF scheme has remained stable for the past few years, ranging from 7.1% to 7.9%. Currently, the rate stands at 7.1% but as per the formula, PPF rates should have been 7.6%.

Why has the PPF rate NOT been increased?

One cannot say for sure why the PPF rates were left behind in the series of rate hikes but here are a few probable reasons –

Tax treatment: Interest rate earned on PPF are tax-exempt. Thus, an effective rate of interest on PPF is lot higher than 7.1%. That could be a reason for not hiking interest rates on PPF further. Interest rates on Sukanya Samriddhi Yojana (SSY) have also been hiked but that could be to promote the social cause of investing for girl children and also because the amount of investments in this scheme is far smaller than PPF.

Push other schemes: The government wants to increase its reliance on the NSSF (National Small Savings Fund) to finance part of its fiscal deficit. The corpus of the PPF was the largest among all savings schemes and this move might bring some parity in the AUM of various other savings schemes.

Cost impact: Among all the saving schemes, PPF is believed to have the biggest overall corpus. So the cost impact of higher interest rates (that too tax free) on the government’s finances is a lot more for PPF compared to other instruments.

Avoid drain on banks: The government cannot hike PPF rates too much as it might make them more attractive than bank deposits. A stead flow of bank deposits is crucial to meet an increase in credit demand that Indian banks are currently witnessing.

Stability: Any significant fluctuations in the interest rate can impact the investments of millions of investors, and the government may not want to disrupt the continuity of the scheme.

Politically correct: The PPF rates remained at 7.1% for a long time even though the yields of comparable govt. bonds were much lower. Now this is because, its far easier to raise the PPF interest rates than reduce it. Whenever there is a talk to reduce it (as it happened in 2021, when the government had to take back its decision to cut PPF rates from 7.1% to 6.4%), there is a lot of negative uproar among the depositors.

Conclusion

The PPF rates may have stayed the same this quarter for various reasons, and there may or may not be a hike next quarter (We can only hope). But we know for sure that PPF will remain a favourite among Indian investors for many years to come as our love for “guaranteed” never ends.