By: Tavaga Research

India’s retail investor is now accustomed to the terminology of mutual funds, thanks to the growing network of digital interfaces and platforms that provide a seamless and hassle-free mode to invest.

That said, collectively, India is far away from what the developed nations have achieved in terms of equity investments. So, even after making so much progress and making strides in financial inclusion, where does India exactly lack? The one-word answer to this question can be sophistication.

An average Indian retail investor has managed to differentiate between various categories of mutual funds, e.g.: Large-Cap, Mid-Cap, Small-Cap, etc. However, the one thing that differentiates us from the developed economies is the selection of best modes to transact when it comes to pooled funds (the majority of US investors prefer passive over active). Further, it gets difficult to segregate between the good, better, and the best, especially if an investor prefers to invest without any advice from a SEBI Registered Investment Advisor.

One of the best practices that team Tavaga honestly believes in is index investing (that too with the help of a SEBI Registered Investment Advisor), especially in the large-cap equity space where market inefficiencies are difficult to find and there is plenty of information available to every market participant.

Therefore, today’s blog circles around one of the best ideas that we would like to share with our devoted readers – The importance of passive exposure to large-cap equity as against active mutual funds and also demonstrate various illustrations of where large-cap (active) mutual funds have struggled to beat the returns of an index/index funds.

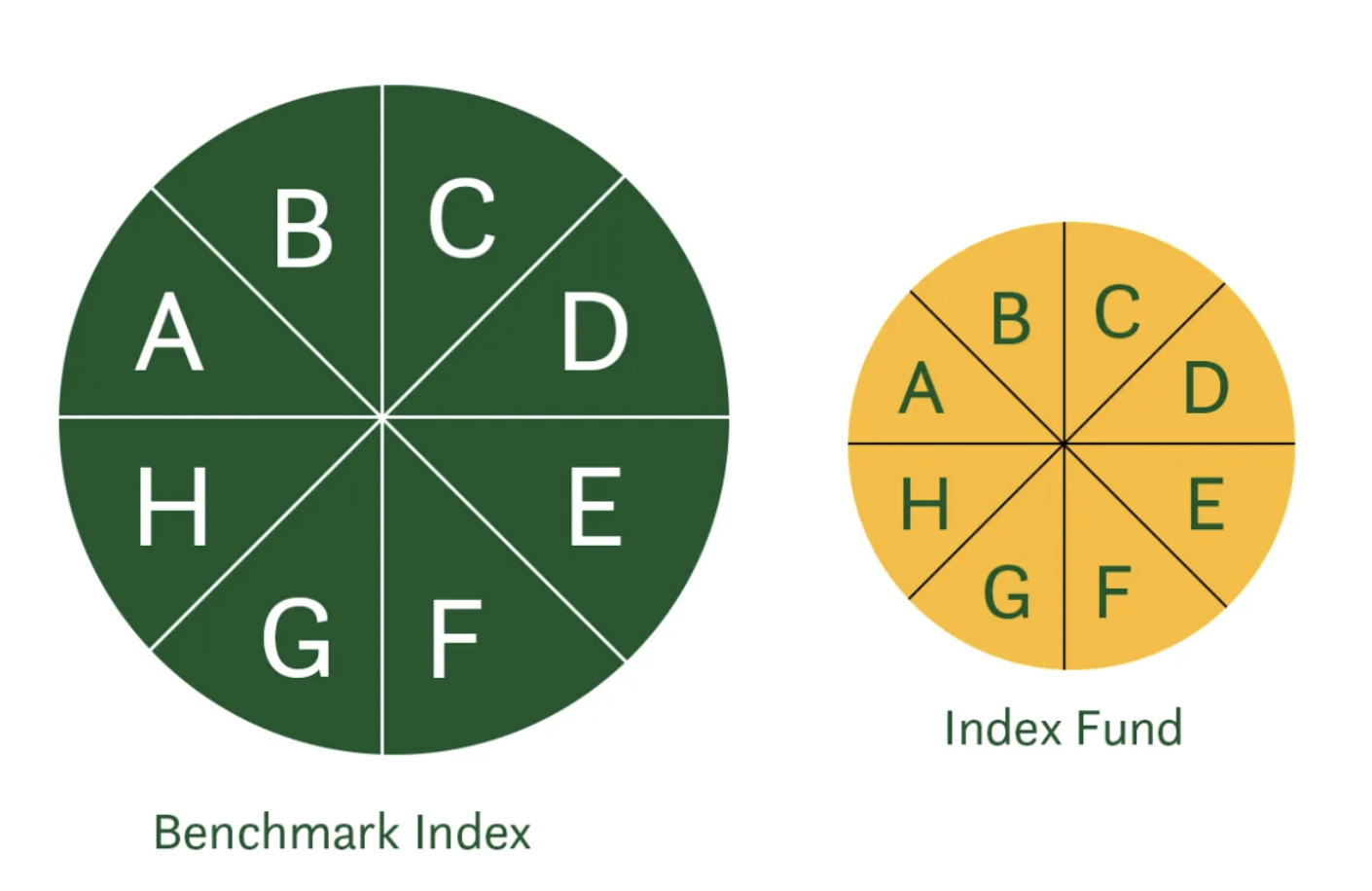

What is Index Investing?

Index investing primarily refers to a method where the investor invests in a mutual fund, specifically a passive mutual fund that tracks a particular index, e.g. Nifty 50, BSE Sensex, etc. It is akin to buying every scrip that is present in a particular index. However, the investor doesn’t have to individually buy every name present in the index, the mutual fund performs that activity and issues a single unit made up of all scrips.

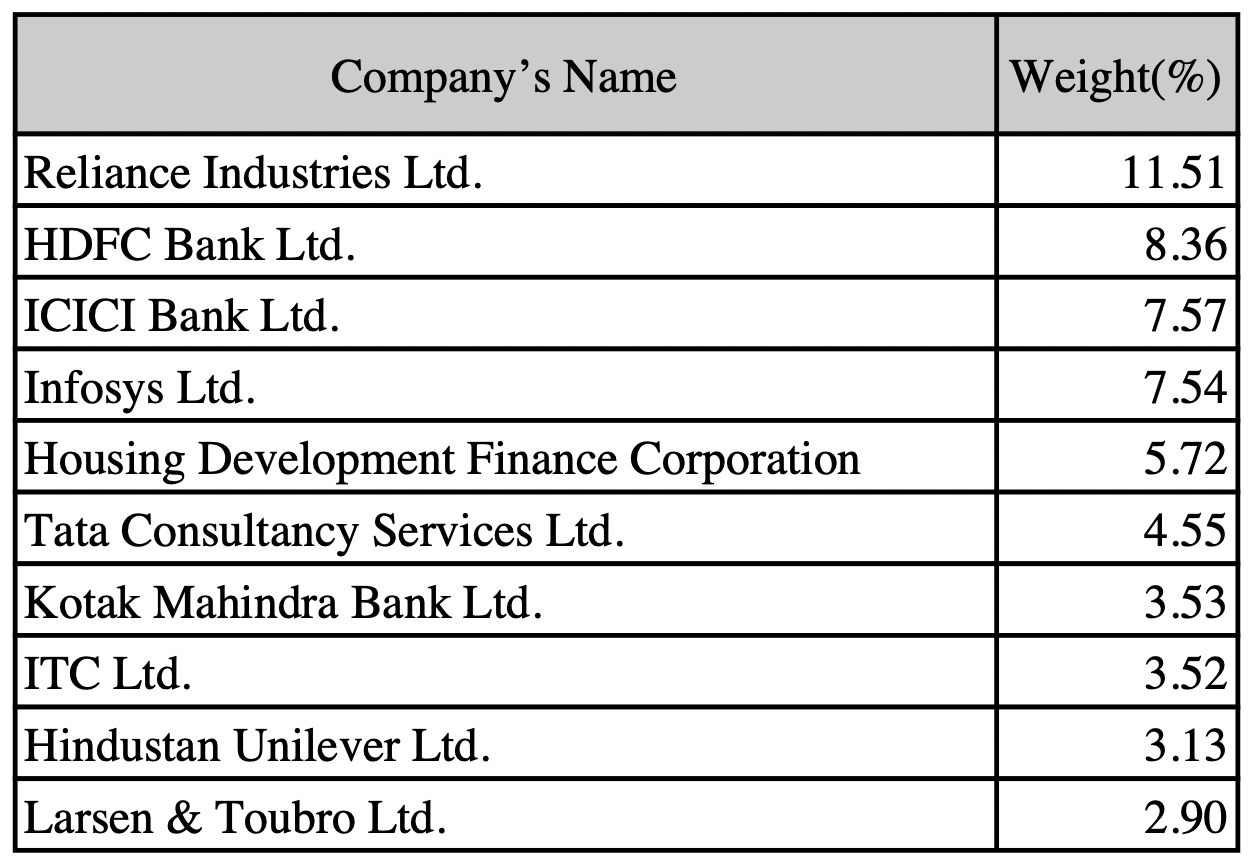

Top Nifty 50 constituents by weightage

Source: NSE

The companies in the above image are the drivers of the Indian economy and almost every investor knows the importance of having them in the portfolio. They are the top constituents of the Nifty 50 index.

What are active mutual funds and passive mutual funds?

Using the above image to demonstrate the difference between active and passive mutual funds, an Asset Management Company (AMC) can provide two techniques to take exposure to the above drivers of the Indian economy.

An active large-cap mutual fund will predominantly invest in the same set of companies albeit with different weights. E.g.: In the above image, Reliance Industries has a weightage of 11.51%. The fund manager managing the active mutual fund might increase or decrease the weight as he/she deems fit.

With large-cap index funds (passive mutual funds), the fund manager will mimic the above image and not modify the weights. E.g.: HDFC Bank will have the same weightage of 8.36% in an index fund as seen in the actual Nifty 50 index.

Examples of Active mutual funds and examples of index funds (passive mutual funds)

| Active mutual funds | Index Funds | Category |

| SBI Bluechip Fund | SBI Nifty Index Fund | Large-Cap Equity |

| Axis Midcap Fund | Axis Nifty Midcap 50 Index Fund | Mid-Cap Equity |

| ICICI Prudential Smallcap Fund | ICICI Prudential Nifty Smallcap 250 Index Fund | Small-Cap Equity |

| Axis Banking & PSU Debt Fund | SBI CPSE Bond Plus SDL Index Fund | Debt |

| Motilal Oswal Flexi Cap Fund | Motilal Oswal Nifty 500 Index Fund | Flexi-Cap Equity |

| ICICI Prudential US Bluechip Fund | Motilal Oswal S&P 500 Index Fund | International Equity |

Coming to the question – Why are large-cap funds underperforming?

In the last few years, AMCs have launched a host of passive funds indicating a shift in the trend of retail investors due to multiple reasons. Passive funds are simple to understand, free from biases of any fund manager, momentum in nature, etc. Well-informed retail investors have taken a plunge by investing in the active mutual fund space in the past and finally moved on to benchmark investing.

So why have the active large-cap funds consistently failed to generate any alpha / outperform index funds?

- SEBI Norms on the categorisation of mutual fund schemes

In the earlier times, there weren’t many categorisation rules laid out by the SEBI. SEBI had given a leeway to AMCs to invest in stocks across various segments of market capitalization. That means, AMCs used to take considerable exposure to mid-cap and small-cap equity despite the nature and ideology of the fund being that of large-cap. A large-cap mutual fund used to take a considerable exposure to mid and small-cap equity stocks. This, in turn, led to high risk and high return, even for the large-cap funds (which is predominantly seen in the case of mid and small-cap funds). However, post-2017, SEBI mandated large-cap mutual funds (Circular No.: SEBI/HO/IMD/DF3/CIR/P/2017/114) to invest a minimum of 80% in large-cap stocks, thus denting the chances of active large-cap mutual funds to outperform the index.

Large-cap equity is generally less risky than mid and small-cap equity as large businesses are well-established and quick to adapt to market dynamics, thus demonstrating low volatility. Mutual fund companies were in a way going against the mandate due to the previous liberal policies of the regulator. Therefore, SEBI’s decision to further regulate the industry was a step in the right direction. However, this is not the only reason for the underperformance of active mutual funds, in fact, the regulation only deteriorated their performance.

- The high expense ratio of active mutual funds

The active involvement of a fund manager in an active mutual fund along with significant churning of the portfolio to pursue alpha often leads to higher costs for an investor. On the other hand, index funds mimic the benchmark. There is no requirement for expertise. Due to the simple nature of index funds, the cost to an index investor, that is, the expense ratio of the index is significantly low. Therefore, active large-cap funds tend to underperform index funds.

| Active Large-Cap Mutual Funds | Expense Ratio | Passive Large-Cap Mutual Funds | Expense Ratio |

| ICICI Prudential Bluechip Fund | 1.05% | ICICI Prudential Nifty 50 Index Fund | 0.18% |

| DSP Midcap Fund | 0.76% | Motilal Oswal Nifty Midcap 150 Index Fund | 0.22% |

| Nippon India Smallcap Fund | 1.02% | Axis Nifty Smallcap 50 Index Fund | 0.25% |

| HDFC Flexicap Fund | 1.06% | Motilal Oswal Nifty 500 Index Fund | 0.40% |

| ICICI Prudential US Bluechip Fund | 2.17% | Motilal Oswal S&P 500 Index Fund | 0.51% |

Comparison of performance: Active Large-Cap Fund v/s Index Fund

- SBI Nifty Index Fund (in yellow) v/s SBI Blue Chip Fund (in blue)

Despite charging a higher expense ratio, the SBI Bluechip fund has failed to provide returns greater than the SBI Nifty Index fund.

2. Kotak Bluechip fund v/s Kotak Nifty 50 index fund (Launched in 2021)

3. ICICI Bluechip Fund v/s ICICI Nifty 50 Index Fund

SPIVA report on active v/s passive

Percentage of Funds that have underperformed the Index

| Fund category | Comparison index | 3-Year | 5-Year (%) | 10-Year (%) |

| Equity Large-Cap | S&P BSE 100 | 70% | 82.26% | 67.61% |

The above table denotes that 70%, 82.26%, and 67.61% of the active large-cap mutual funds have underperformed the S&P BSE 100 index over a 3-Year, 5-Year, and 10-Year horizon, respectively. Thus, the majority of the active funds have consistently underperformed the underlying index.

Tracking Error – The only pitfall of investing in an index fund

Tracking error measures the difference between the index fund performance against the underlying benchmark it tracks/mimics. With passive investing, an investor is investing in a fund that is replicating the benchmark.

At times, there are chances of the fund failing to completely replicate its benchmark and this may give rise to a high tracking error. The lower the tracking error, the better it is for the index fund. Again, choosing an index fund with the lowest tracking error doesn’t always solve the problem. That particular fund that had the lowest tracking error in the past could well fail to perform in the future.

An investor must keep in mind that jumping the ship just because of a change in tracking error isn’t the optimal solution. The tracking error has to be always compared with its peers and the decision to liquidate or change the fund should be only taken if there is a consistently higher than industry average tracking error.

Thus, team Tavaga believes that large-cap index funds will continue to do well against the large-cap active funds, in the future. There can be times when an active fund does well in a particular year, but on a longer time horizon (which equity investors generally tend to have), passive investing is the way forward!

The best way to transact in an index fund would be to do SIPs. During market downturns, buying lumpsum in a staggered manner will fetch good results for the investor.

Tavaga is everything you need to start saving for your goals, stay on track, and achieve them in time.

Download Now: