If you have been following the news, you may have come across the surge in activity within the Indian Aviation space. From the launch of the new Akasa Air to the reboot of Jet Airways, the skies are finally beaming with hope post-pandemic. Let’s dive deeper to understand the new bustle in the sector and how the new developments will shape the future of the aviation industry in India.

Overview of the Indian Airline Industry

Currently, India is the 7th largest civil aviation market and is all set to become the 3rd largest with the rapidly growing working and middle-class population. The market leader is the low-cost carrier – Indigo which holds a whopping 54.8% market share as of December 2021. But the competitive landscape is slowly changing.

Let’s unravel the recent developments in the Indian Airline Space.

- Tata-owned Air India and Vistara are planning to merge their operations under one single brand.

- India gets a new airline within the low-cost carrier space with the launch of Rakesh Jhunjhunwala’s Akasa Air.

- After Jet Airways had filed for bankruptcy in April 2019, it is back in full motion to fly the skies once again.

Why are the skies buzzing with activity?

If we recall, Rakesh Jhunjhunwala, a well-known investor came out with Akasa Air in a not-so-good weather amidst high fuel prices, covid restrictions, failure of Jet Airways and unending debt burdens on airline companies. So, what really made the big bull and other companies deploy funds in the bleeding airline industry.

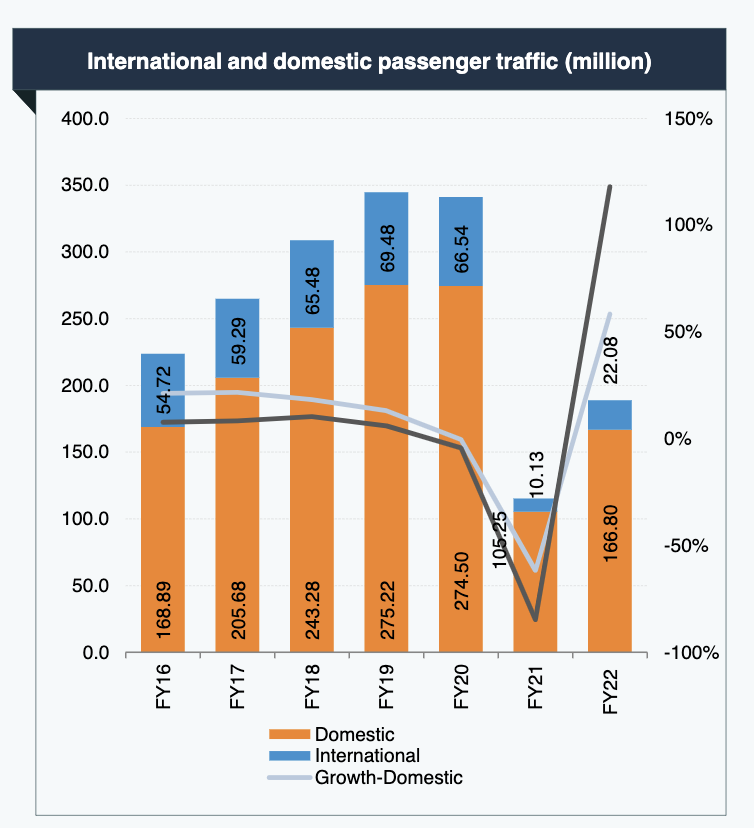

Low penetration: Aviation penetration in India remains among the lowest in the world. For instance, the total fleet size in India was 716 as of December 2020 while the fleet size of American airlines alone is 994. So, there’s good scope for companies to expand their business.

| Airline | Fleet Size |

| Indigo | 276 |

| Air India | 256 |

| Spicejet | 91 |

| Go First | 57 |

| Vistara | 54 |

| AirAsia India | 28 |

| Akasa Air | 4 |

Advantage India: India is home to a large young and working population. Rising travel demand from domestic and foregin tourists, business and leisure travel and the growth in external trade is the silver lining for the industry. In fact, growth in demand has consistently outpaced the growth in supply, resulting in a high Passenger Load Factor.

Domestic Airlines: Passenger Load Factor

Source: CEIC Data, DGCA

The government, too, is playing its part by introducing initiatives that would improve infrastructure, increase regional connectivity and bolster FDI and private sector participation. It has also been promoting its ‘Open Sky Policy’ which would enable airlines to operate unlimited direct flights to any country.

Post-pandemic demand: Airfares on popular routes have crossed the pre-pandemic levels and the daily number of domestic air passengers touched 4 lakh as consumers indulged in revenge travel after facing a host of restrictions in the last two years. This is the right time for airlines to recoup their losses by cutting down on promotions and increasing revenues.

How will the new developments change the airscape?

The merger of Air India and Vistara can be a deal breaker for the industry. It could present a new flag carrier for the country – combining Air India’s extensive fleet and valuable slots with Vistara’s renowned soft-product offering. Given a fleet size of 300+ post merger, it could also give finally give stiff competition to Indigo and may even dethrone Indigo from its market-leader position and build a strong footing against the Middle east dominated international traffic.

Competition is set to be even more cut-throat within the low-cost carrier space with the launch of Akasa Air. Price wars have already begun with Akasa Air cutting prices across its routes. For instance, seats that went for about Rs. 5000 on the Mumbai-Ahmedabad route are now being sold for just Rs. 1400! As a result, the country’s largest airline, IndiGo is also cutting its fares on these routes.

And this comes at a time when the sector is trying to recoup its previous losses. With Covid restrictions wading away and removal of fare caps by the government, airlines thought it was the right time to focus on reducing costs and increasing revenues. But with the antics of Akasa, it’s putting a further dent on the wallets – especially low margin carriers. Now, has it started to make sense of the Big Bull’s decision to enter the Ultra low-cost space?

The bottom line

Given the predicted rise in travel demand within the next decade, the outlook for airline operators looks favorable. In the near term, however, the airline industry is poised for a turbulent period of rising competition and pricing pressures. This brings up an important question whether all the players will be able to survive the intense competition or will they be forced to pack their bags like the dormant Kingfisher.