The face of financial transactions and access to financial services has potentially been revolutionized in early September 2021, when a new technology infrastructure Account Aggregator (“AA”) was launched at a virtual event wherein 8 largest banks of India namely, State Bank of India, ICICI Bank, Axis Bank, IDFC First Bank, Kotak Mahindra Bank, HDFC Bank, IndusInd Bank and Federal Bank came together to join the network for a smooth and centralized transition of financial data.

Account aggregators are a subset of non-banking financial companies (“NBFCs”), which function as technology intermediaries between entities requiring financial data of customers (financial information users “FIU”) and those holding that data (financial information providers “FIP”).

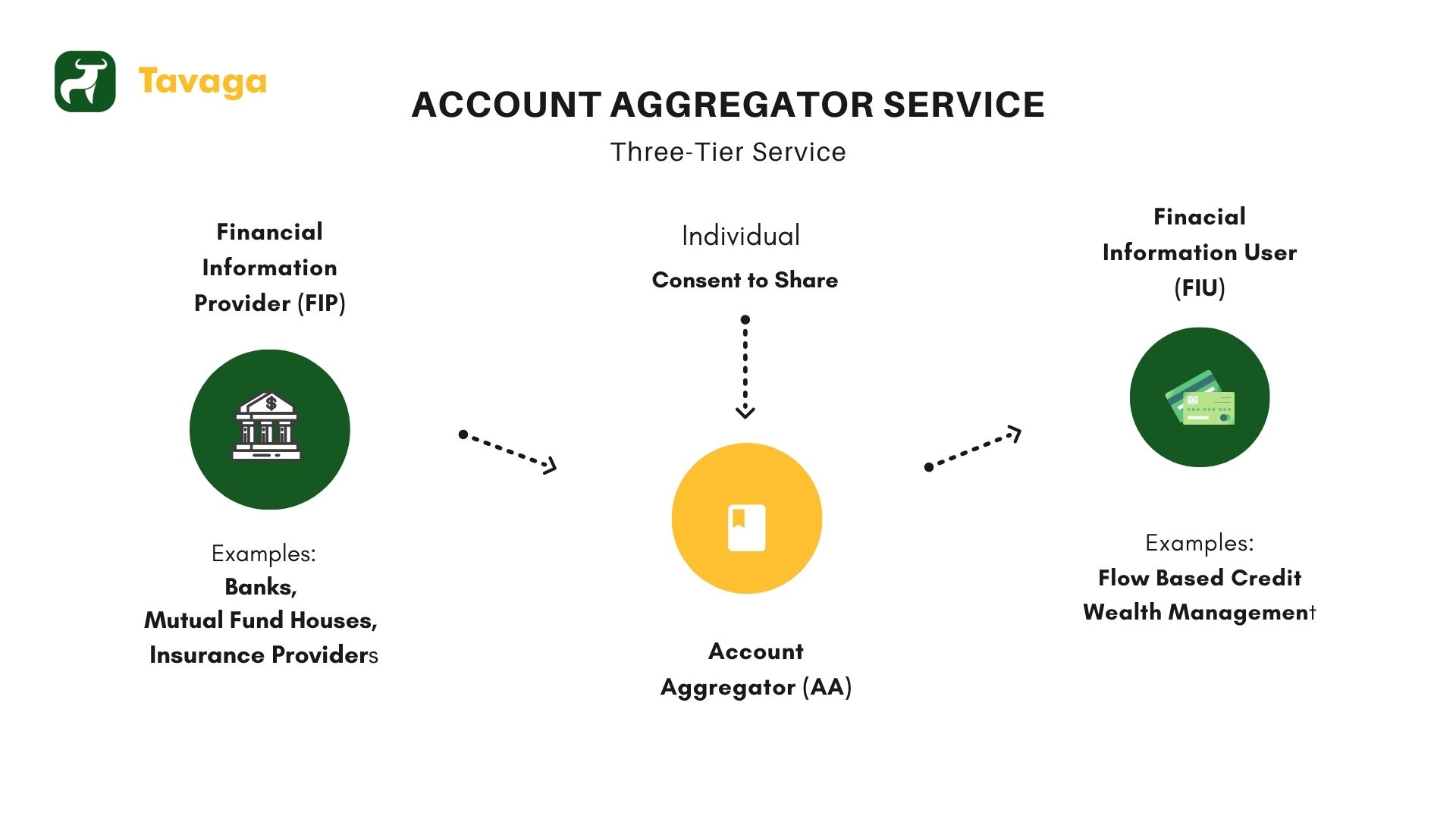

Simplifying AA –

The whole process has a three-tier structure and the license for AAs is issued by the RBI. These will help in facilitating financial data of customers to FIPs and FIUs which include banks, lenders who do not delve into banking, insurance companies and mutual funds, who seek financial data and documents from their customers. Information scattered across all of the financial institutions that one deals with will be stored via a centralized mechanism and shared to an FIU if the customer consents for the same. Thus all the digital footprints of the customer will be compiled in one place and facilitate the information acquisition to lenders. At least four banks, including HDFC Bank Ltd., ICICI Bank Ltd., Axis Bank Ltd. and IndusInd Bank Ltd., have started the AA services for a small set of customers before they open up these platforms to everyone.

How is AA Revolutionary?

1. Improved Financial Understanding: The most pertinent benefit of an Account Aggregator service is the ease with which customers can analyze financial information to make well-informed decisions with regards to their banking and investment choices.

2. Less Turnaround Time: AAs essentially cuts down the enormous amount of time that customers have to undertake in order to avail of a financial service, and thus the hassle to run around and collect all the financial documents before availing of financial services will be done away with. This time saved could be rather invested into analyzing the services provided by various competitors in the market!

3. Less physical interactions: COVID-19 has been a major roadblock on physical restrictions and end-users are afraid to visit banks and other financial offices. This can be potentially solved by an AA that creates secured digital access to personal data. To cite an example, data sharing through AA to procure information collateral can be used to access a small formal loan by MSMEs who generally ask for physical collateral.

4. Fraud Reduction: It reduces the fraud associated with physical data by introducing secure digital signatures and end-to-end encryption for data sharing. Further, the services of third parties cannot be used for undertaking the business of account aggregation. Moreover, the consent of the customer is at the core of the AA ecosystem. Thus, if a person decides to not share the financial data, it will stay with the finance provider. According to Sahamati, a collective AA ecosystem, an AA is “data-blind” which essentially means that all data transferred is encrypted and could only be accessed by the FIU for which the data is intended. Also, an AA has not been authorized to store any user’s data. Consequently, user data is prevented from being misused or from potential leakage.

5. Synergy between Unified Payments Interface (“UPI”) and AA: With the onset of UPI, payments have become increasingly accessible and pervasive. The AA system works on a similar idea, the only difference being in the data which is being exchanged. The technology-driven payment services application allowed customers to exchange payments on several banking accounts via a single application by a virtual payments address, with each having a unique separate identity. The AA entities will also follow suit of the UPI payment mechanism and will enable a user to transfer numerous financial data held by the user in multiple accounts (saving accounts, term deposits, mutual and pension funds etc.) through a single virtual address exclusive to each user. This will be shared to an FIU, provided the user consents to the same along with granting access to particular information which has been requested through an AA identifier.

Potential Loopholes of AA:

- Data Ethics and Data Mining

Although the idea of AA is lucid, issues such as data ethics and data mining for private profits could serve as major roadblocks towards the transparent financial data sharing process. The AA system could be used peripherally for data mining by FIPs and FIUs.

To simplify this, suppose a food delivery entity such as an online food entity starts offering purchase food on credit. It could thereafter ask the customer to enrol into a programme wherein the customer is required to share income and account statements to confirm your creditworthiness. Sharing such details through an AA would mean that the food delivery entity can now get an insight into your previous purchase history. They might use this information for targeted advertising. Thus, if one has purchased a lot from Chinese restaurants, food entities will advertise more Chinese food and restaurants even though one has never ordered Chinese food from that particular food entity.

- Data Security

The abundance of personal, sensitive and confidential data also inevitably leads to data security challenges, where hackers may obtain unauthorised access to an account aggregation site and steal sensitive information to undertake a transaction or engage in other fraudulent activities. Even a single point of failure will prove cataclysmic towards the financial ecosystem. To overcome the same, enormous IT capabilities across the AA ecosystem entities are required to handle aspects like technology and UI/UX design and data warehouses, in addition to cyber security and privacy frameworks.

- Financial Literacy

India has had a unique trend wherein even though numerous attractive schemes, policies and services are released, they are not utilized to their full potential. This occurs primarily due to the lack of penetration of financial literacy in India. A classic example for the same is Pradhan Mantri Jan Dhan Yojana. Studies have shown that people who are eligible under the PM-Jan Dhan Yojana have still not opened a bank account due to the lack of awareness regarding the same.

Thus, in order to make AAs more accessible to communities who are genuinely in need of the same, policies regarding financial literacy must be implemented. With regards to literacy about Account Aggregator Services, substantial steps have been taken. Sahamati is a collective of AAs established by a private limited company (under the new Companies Act of India, not-for-profit companies are governed under Section 8). It will be connected with numerous FIPs, which includes banks, insurance providers, mutual fund houses and even Tax Departments to advocate for the AA system and create awareness for the same. With a stringent policy at hand, the need of the hour is its proper and judicious execution.

Is it really revolutionary?

The ecosystem has the potential to serve as the holy grail of financial services providers and customers alike, provided its execution is done immaculately. AA mechanism can achieve meteoric success if all financial services providers, as well as government entities such as Income Tax and GST and other business entities, are on the platform. It is not compulsory for every financial service provider to partake in the AA ecosystem as of yet. However, it is mandatory for an entity that wants to become an FIU and provide more personalised services to its customer base to become a FIP as well ‒ that is, it should be willing to share its customer’s data (with customer consent) with other FIUs.

Tavaga is everything you need to start saving for your goals, stay on track, and achieve them in time.

Download Now: