Decoding Crypto as Commodity

Governments around the world have struggled in coming up with regulations for Cryptocurrencies. Many-a-time it has been pointed out that cryptocurrencies may disrupt the entire financial system and this only makes it more urgent for the Governments to come up with a solution to harness the Cryptocurrency Market. One of such ways has been envisioned by the Government of India in the new draft bill to declare Cryptocurrencies as a commodity.

The main aim of this bid by the Government is to regulate the wildly unregulated Cryptocurrency environment and to make way for the new CBDC (Central Bank Digital Currency), which will be discussed further in this article.

Cryptocurrencies need no introduction in today’s day and time. These are a form of currency or a digital asset that is unique. Cryptocurrency uses a technology called blockchain to form a decentralized network of currency that many users claim serves as a hedge against inflationary tendencies.

It is important to understand the role of cryptocurrency as a commodity/asset if this alleged new draft bill is tabled and gets passed. The current global market cap for Cryptocurrencies stands at $2.26 Trillion, given the growth of these digital assets it was only natural that governments take some measures to control them. Treating Cryptocurrencies as an asset will open a plethora of avenues for the Govt. to regulate them, tax them and reduce some uncertainties surrounding the Cryptocurrency Environment.

Until now cryptocurrencies were not classified which made it virtually impossible to tax. With their possible classification as commodities or assets under this alleged bill, they are open to being taxed like one. In one of our blogs, we have discussed at length the possible taxation regime in case Cryptocurrencies are classified as assets. It is still under speculation whether this probable bill layout a completely new taxation scheme, specific to these digital assets or any income arising out of them will be treated the same way as it is treated in the case of existing assets and commodities.

CBDC: A Boon or A Bane

In addition to the news of the probable declaration of Cryptocurrencies as commodities, the RBI Deputy Governor, T Rabi Sankar spoke about bringing the CBDC to the Indian Financial Space. CBDC has been a point of great discussion in the recent past. Governments see CBDC as a potential deterrent against the growing influence of a completely unregulated crypto environment and to stay ahead of private influence on monetary politics.

CBDC’s are a form of virtual currency with the same value as fiat currency. CBDC is based on the same Blockchain technology used by all the cryptocurrencies. Since no actual CDBC has been launched until now, the form they will take can only be speculated. One thing everyone can place their bets on is that, unlike conventional cryptocurrencies, the CBDC would be based on a private blockchain network given the fact the Central Banks would want to protect the transactions happening every day from the eyes of bad actors in digital space.

Over the course of the last year, many countries have dabbled with the idea of introducing the CBDC. According to the Bank of International Settlements (BIS) report, over 80% of Central Banks are already researching CBDC. Forerunner in the development race of CBDC’s China is leading the race with its Digital Yuan, followed by Sweden with its e-krona. Moreover, in the US a counter-proposal was offered to the Stimulus package, it referred to the possibility to introduce a digital dollar account maintained by a Federal reserve bank to deliver benefits in response to the pandemic crisis.

However, while the debate and research on how to design a CBDC are still heated, little attention has been paid to the consequences of introducing a CBDC from an Indian financial landscape and policy perspective.

Why can CBDCs not be a reality soon?

Conceptually, CBDC’s are a perfect form of digital currency. It offers the following:

1. Provides security against the volatile fluctuations unlike cryptocurrencies as they are backed by the Central Bank

2. Valid legal tender.

3. Helps the government curb tax evasion and fraud.

4. Universally Acceptable.

5. Financial inclusion of the unbanked and the underbanked as no bank accounts will be required to be set up.

All these characteristics make some good arguments for the government to go forward with the implementation of the CBDC. But there are more disadvantages to the implementation of CBDCs than advantages.

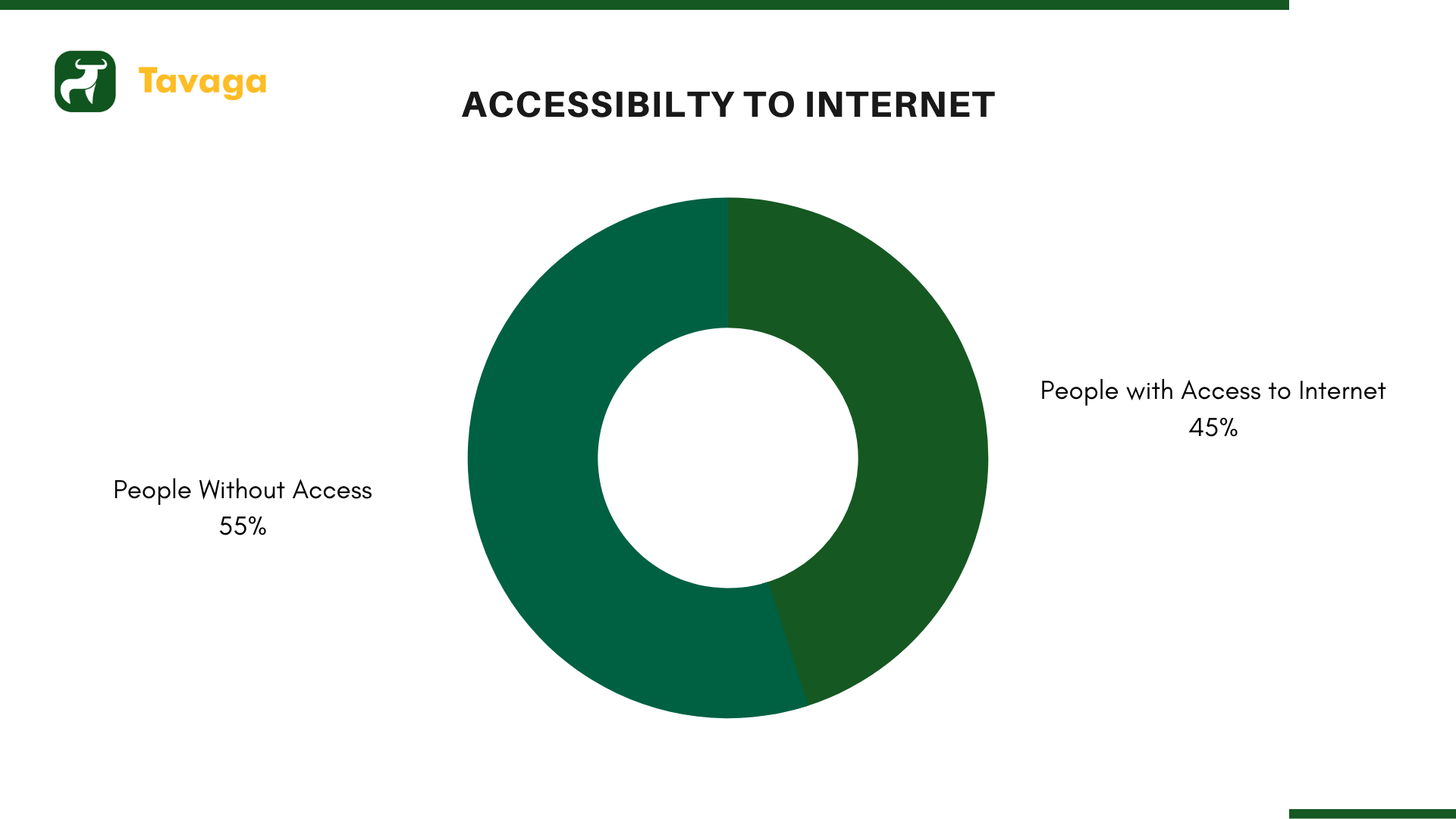

1. Financial Inclusion: An argument regarding the Financial inclusion of the unbanked and the underbanked is made in support of the CBDCs. In reality, the financial inclusion of these people depends mostly on the digital penetration in the country. According to a report, digital penetration in India stood at 45% in January 2021. This figure alone is enough to make an argument against the rollout of CBDCs as it would leave out almost half the population of the country to reap the possible benefits of this digital currency. Further, the existing banking structure is very robust and has taken very deep roots in India, people with little or no financial knowledge usually prefer a personal touch if any queries/problems arise and are generally dependent on the advice of the bank personnel.

2. Lack of Trust: People in India usually do not trust digital payment methods. Taking an example of UPI, according to an NPCI Report, since its launch UPI has only garnered 100 Million users which is a really small number in a country of over 1.3 Billion people.

3. Lack of Financial Literacy: The Indian population has a long way to go in gaining basic financial know-how. Even the country’s literate population is averse to engage themselves in a plethora of financial services or payment systems that already exist due to the financial and legal jargon. Language plays a great part in educating people about the financial landscape. Linguistics are a major roadblock in a country like India.

4. Data Protection and Privacy Concerns: Data Security is a major concern in India, with the rampant increase in digitization in the last 2 years, the data breach has become a major issue. The abundance of personal and financial information that the CBDC accounts will be huge. Even a single point of failure or vulnerability will prove to be devastating. For the CBDC to become a reality anytime soon, the Digital Infrastructure must be improved leaps and bounds. Additionally, CBDCs will run on private blockchain networks, which in turn will give full access to the Central Banks to every financial activity of every individual, essentially leading to an Orwellian monitoring space.

Conclusion:

Looking at these two new possible developments from a bird-eye view, it can be clearly seen that the two are complementary to each other. With the news of possibly classifying existing cryptocurrencies as commodities in conjunction with T Rabi Sankar’s statement on CBDCs, one cannot help but speculate the intention of the regulators pertaining to the future of cryptocurrencies. Although the CBDC cannot be a reality in near future, one thing that can be said for sure is that the stance of the regulators is softening towards cryptocurrencies.

Tavaga is everything you need to start saving for your goals, stay on track, and achieve them in time.

Download Now: