By: Tavaga Research

With the second IPO of the season, Adani Wilmar is ready to issue equity shares worth Rs 3600 cr. Here’s the list of 10 things that you should consider before investing in the IPO.

- Business Model

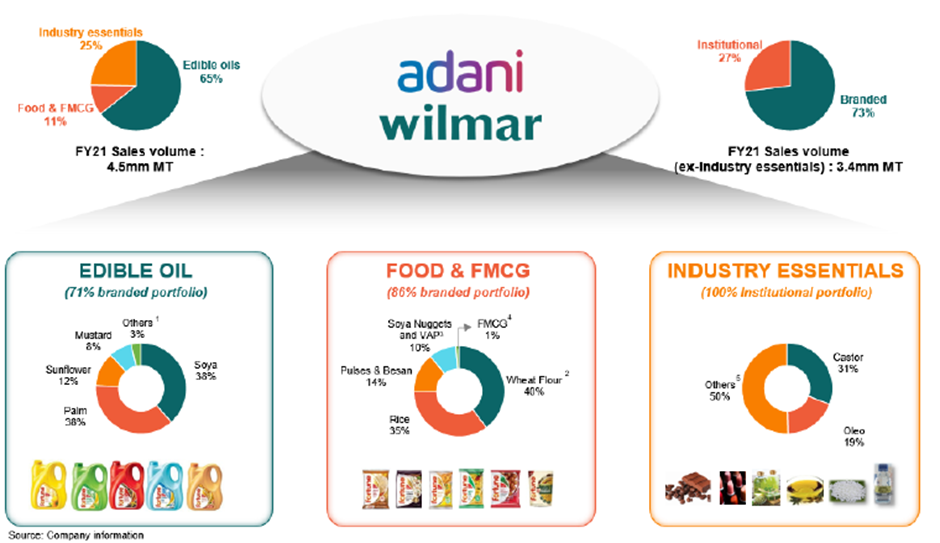

Adani Wilmar is one of the leading FMCG companies in India, offering essential kitchen commodities and catering to all spectrums of consumers across India. Essentially, it sells edible oil, wheat flour, rice, pulses, and sugar under a diverse range of brands with a broad price spectrum.

Source: DRHP

The company was set up in 1999 as a joint venture between Adani Group and Wilmar group. The Adani Group is a multinational company operating into diversified business segments such as logistics and transport and energy and utility sectors, while Wilmar Group is Asia’s largest agribusiness group based out of Singapore. The Adani Wilmar group benefits from strong parentage, Adani’s in-depth understanding of local markets, logistic capabilities, and Wilmar’s sourcing network capabilities and technical know-how.

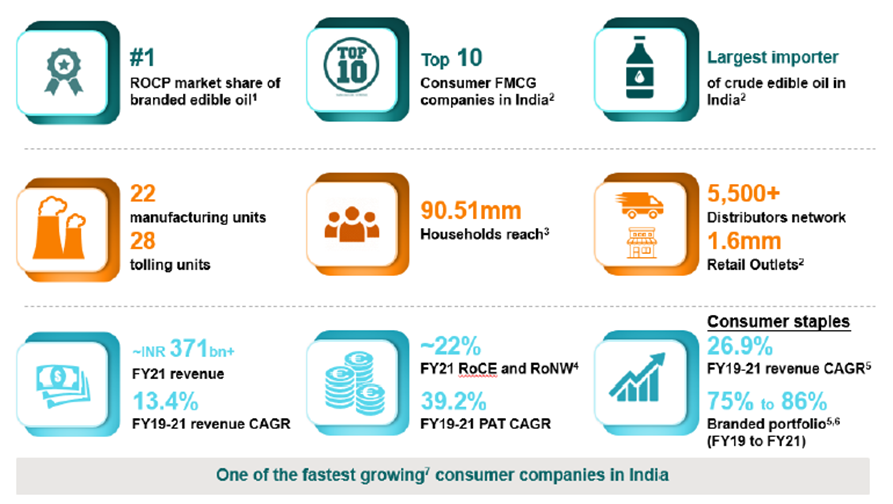

Currently, the company is operating 22 plants across 10 states across India, comprising 10 crushing units and 18 refineries. As of March 31, 2021, the FMCG giant has used 28 leased tolling units, increasing its manufacturing capacity. The company Mundra refinery has a total capacity of 5000MT per day and is one of the largest single-location refineries in India.

The company’s product portfolio comprises three categories – edible oil, FMCG and packaged food, and, lastly, industry essentials. The Fortune brand, its flagship brand, is the largest edible oil brand in India, and it’s also one of the fastest-growing packaged food companies in India as per growth in revenue for the last five years. Lately, the company has been looking into value-added products to diversify its revenue streams and launched functional edible oil products, such as rice bran health oil, ready-to-cook soya chunks, fortified foods, khichdi, and FMCG.

The company has adopted backward and forward integration and integration of manufacturing units for edible oil and packed food to save on expenses and be cost-efficient. Other than that, the company has a strong network of distributors located in 28 states and 8 UTs in India, catering to 1.6 million retail outlets.

- Industry

With the advent of modernization and changes in the lifestyle of people, the FMCG has become the fourth largest sector in India, with 50% of sales being generated from households and personal care products. The urban population has always been the major contributor to the sector’s revenue, accounting for 55% of the revenue as of November 2021. However, demand is growing faster in rural areas than in urban parts of India because of the growing awareness and easier access to products.

Statistics reveal that the FMCG market will be USD 220bn in 2025 from USD 110 bn in 2020, showing a CAGR of 14.9 %. Even the packed food market in India is expected to double to USD 70bn by 2025. Rising digital connectivity is the driving force behind the positive growth prospects of the industry.

Rural India provides plenty of opportunity through rising disposable income and a low level of penetration of outlets in those markets. Moreover, the estimates reveal that the e-commerce segment will likely contribute 11% to the overall sales of FMCG by 2030.

Due to the Covid pandemic, the demand for packed food has increased however the demand in Indian households remains limited. Compared to China and USA, the annual per capita spent on all packaged food categories remains low in India, equivalent to Rs 4650 in relation to Rs 16000 in China and Rs 112500 in the USA.

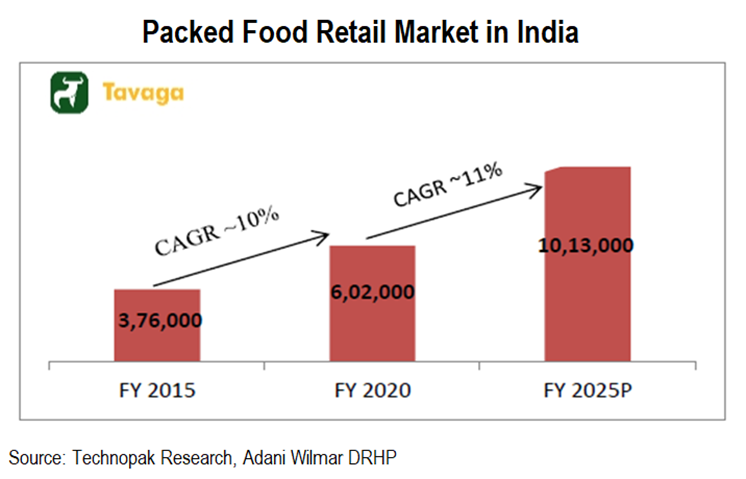

The sector is expected to grow at CAGR of 11% from Rs 6,02,000 crore in FY2020 to Rs 10,13,000 crore in FY2025.

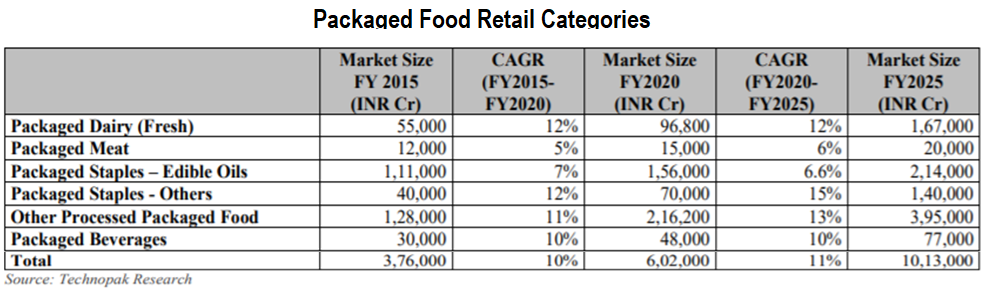

The table below shows packaged food retail categories; edible oil grew at 7% from FY2015-2020 and is expected to grow at 6.6% from FY2020-25, which is reasonable. Overall the market will grow 11% from FY2020-25.

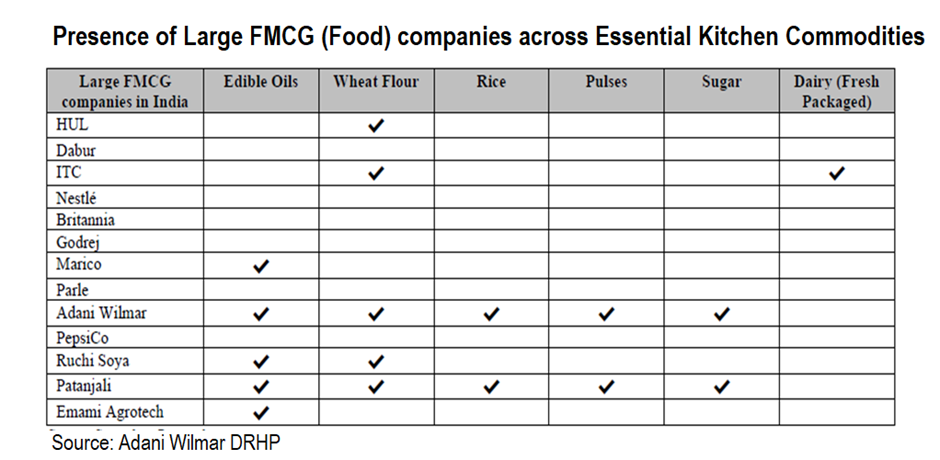

In the Essential Kitchen Commodities, most players are focusing on either one or two categories of products, while few players like Adani Wilmar and Patanjali have a presence across almost all the major categories.

In the Branded Edible oil market, Adani Wilmar holds the largest share of the pie, equivalent to 17% of the total market share.

- Use of Proceeds

- The company will utilize Rs 1900 crore on capital expenditure to develop new manufacturing facilities and expand existing ones.

- Rs 1058.9 Cr. for repayment of loans

- For funding strategic acquisitions and investments, Rs 450 cr

- For general Corporate purposes, Rs 191.1 crore.

- Financials

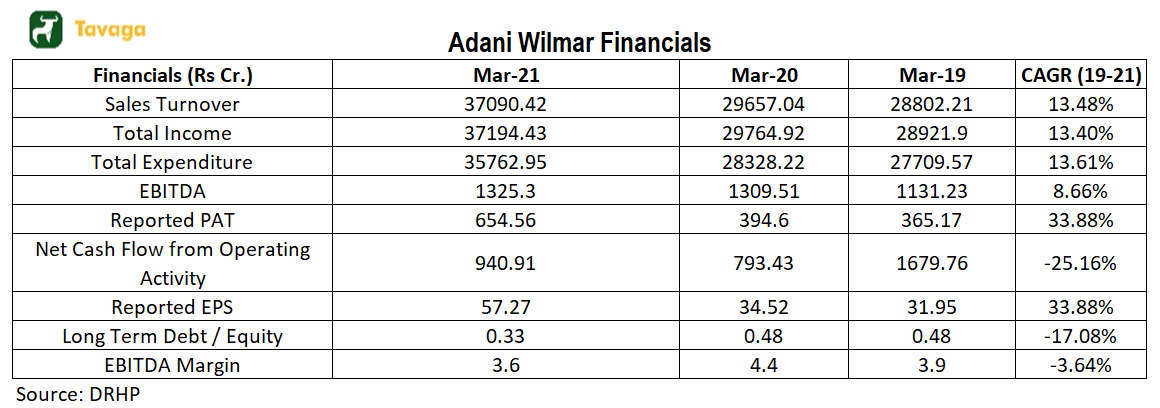

The revenue from operations showed a CAGR of around 13% from 2019–21. EBITDA has also grown by 8.66% from Rs 1131.23 cr in FY19 to Rs 1325.3 cr in FY21. PAT has increased significantly from Rs 365.17 cr to Rs 654.56 cr having a CAGR of 33.88%.

While the company continues to generate cash flows from its core operations, it needs to further improve upon this metric. A sales and profit growth is considered as healthy only when the company manages to consistently generate cash flows from its core operations.

- Risks

- The business is dependent on a large number of raw materials such as unrefined palm oil, wheat, paddy and oilseeds, soyabean oil, and sunflower oil; however, unfavorable weather conditions can hamper the availability of raw materials.

- Its operations majorly depend on raw material imports or domestic supplies; various factors can result in insufficient supply of raw materials or lead to a rise in its prices which can be a risk factor for the business.

- Some of the company’s promoters are involved in legal and regulatory proceedings, which can impact its reputation.

- The company derives a huge chunk of revenue from the edible oil segment; any losses on that front could create an adverse problem.

- Prices of products sold by companies fluctuate due to many factors such as world demand and supply, weather, trade disputes, raw material supply, governmental regulations, among others.

- Advantages

- The company has strong brand recall value; fortune is one of the largest edible oil brands in India

- The company has leadership in branded edible oil; the company caters to 17% of the market share

- Strong Parentage, as it’s a JV between Adani and Wilmar Group, both have a strong foothold in specific areas

- Wilmar is the largest palm oil supplier in the world, which protects from price risk

- Adani Wilmar is the largest edible oil importer, creating bargaining power for better raw materials quality.

- The company has one of the largest distribution networks; it is present in 1 out of every three households, according to the IMRB report.

- Valuation

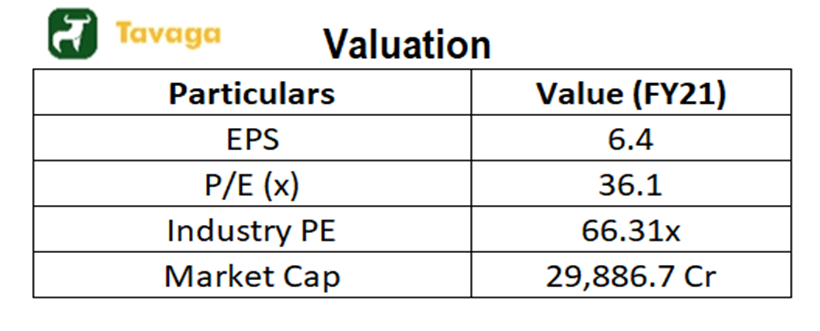

On the earnings multiple front, Adani is coming out with an issue at 36.1x (at upper end of the price band).

On an industry-wide basis, it comes at a relatively attractive price, however, with not that high margin of safety. Moreover, with inflation setting in, consumption companies could take a massive hit and no more enjoy the comfort of high P/E multiples.

- Peer Analysis

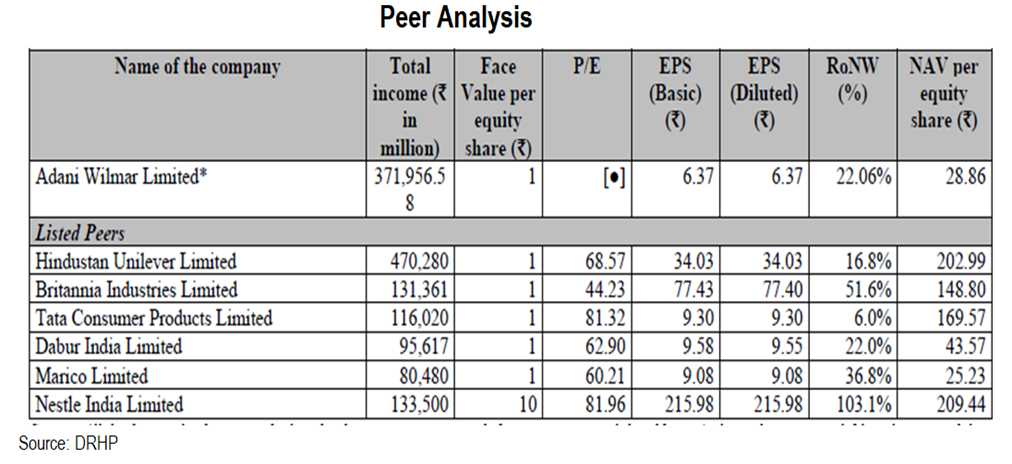

The trailing P/E ratio of the company is 36.1, which is the lowest compared to its listed peers; Britannia has a P/E ratio of 44.23, while others have a higher P/E ratio above 40. It can mean that the price may be undervalued and that there’s some margin left for listing gains as far as P/E metrics is concerned.

The company has a fairly decent RoNW at 22.06%, the fourth largest among its peers. Generally, RoNW lower than 15% is considered harmful, suggesting the bad financial position of a company. It is calculated by dividing Net Income by shareholders’ equity.

- Anchor Investors

The company has decided to allocate 4.08 crore equity shares to anchor investors at Rs 230/share. Anchor investors are Qualified institutional investors making an application for Rs10 crore or more. By investing in shares, anchor investors boost investors’ confidence and attract them to subscribe for IPO.

Adani Wilmar has collected Rs 940 crore from Anchor investors. Government of Singapore, Monetary Authority of Singapore, Jupiter India Fund, HDFC Mutual Fund (MF), Societe Generale, Nippon India MF, and Aditya Birla Sun Life MF were the major anchor investors.

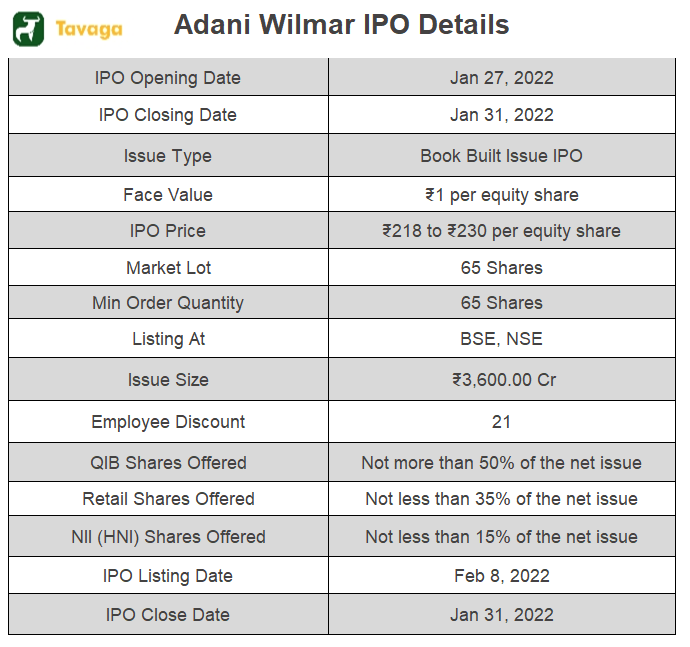

- IPO Details

Ending Note

Adani Wilmar is undoubtedly one of the largest FMCG players in India, focusing on kitchen essential Items within the Packed food range. The company is a 50:50 joint venture between two strong players Adani and Wilmar Group in their respective fields. Hence the Adani Wilmar has a strong parentage which provides many advantages in local markets raw material sourcing, among others. Moreover, the company’s financials present a positive picture for further growth in the FMCG segment. The company earns most of its revenue from the edible oil segment, with the famous brand Fortune providing a solid brand value.

The FMCG Industry also has a huge growth potential due to easy availability, changing lifestyle, and digital drive. However, one needs to be careful about the risks gleaming at the bounds of the company as it can be affected by several factors leading to losses such as global demand & supply fluctuations, prices of raw material and its availability. The company’s strategy is to expand its manufacturing units, launch diverse products and services in FMCG, and become a household name for its various products.

All in all, one must take an informed decision based on points discussed above and after consulting his/her SEBI Registered Investment Advisor.