By: Tavaga Research

India is known for its rich culture, festivities, weddings, and heritage. One of the things which keeps the enthusiasm alive is the vibrant attire and colorful fabrics available for all kinds of Indian festivities.

Manyavar (Vedant Fashion), as we all know, is a popular men’s wedding attire brand whose parent company is planning to roll out an IPO to enter the stock market. The IPO consists only of an offer for sale of 3,63,64,838 equity shares. The offer’s price range has been set at Rs 824-866 per equity share. Here are ten things to know before buying into its shares.

1. Business Model

Vedant Fashions, founded in 2002, provides Indian wedding and celebration clothing for men, women, and children through an omni-channel network of 546 exclusive brand outlets (EBOs), 825 multi-brand outlets (MBOs), and 145 large-format shops (LFS) as well as online platforms. The company operates on a franchisee-owned-company- operated (FOCO) basis.

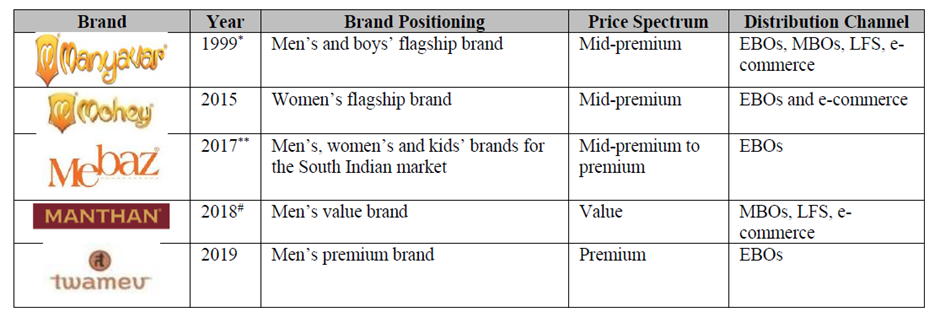

Manyavar (men’s brand), Twamev, Manthan, Mohey, and Mebaz are among the company’s multi-brand product portfolios. Moreover, its famous brand Manyavar is a category leader with a pan India presence in the branded Indian wedding and celebration wear market.

Vedant fashions have set its mark as the most prominent Indian company in the men’s Indian wedding and celebration wear segment in terms of revenue and profit after tax for 2020.

The company has established its diverse brands by identifying gaps in the underserved and high-growth Indian wedding and celebration wear category. It operates through multiple channels networks and offers a diverse range of products catering to customers in value, premium, and mid-premium segments (Source: DRHP).

The company is asset-light and doesn’t require heavy plant, property, and equipment; due to the nature of its sourcing and manufacturing operations, hence it’s able to generate a high return on capital employed. Furthermore, economies of scale and minimal investing in manufacturing and distribution networks can easily optimize production, procurement, distribution, and employee costs.

As of 30 June 2021, the retail footprint of the company reaches 1.1 million square feet including 525 EBOs across 207 cities and towns in India and 12 EBOs overseas.

Moreover, customers have the option to place orders through online channels such as the company’s website, mobile application, and e-commerce platforms as well.

In FY 21, Franchise owned EBOs generated 44.22% of the sales from Tier 1 cities, 42.05% from Tier 2 cities, and 12.31% from Tier 3 cities; the remaining sales were generated from international markets.

According to FY 2020 data, Indian wedding and celebration wear forms 57% of the overall ethnic wear market.

2. Industry

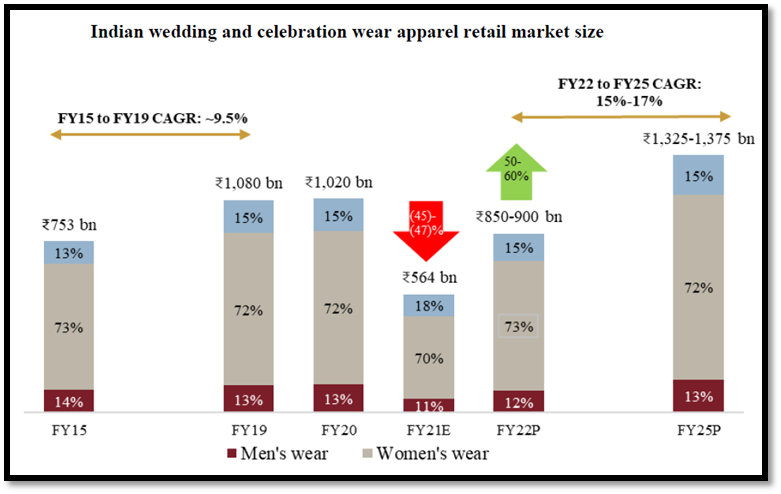

Statistics reveal that from 2015-to 2019, the Indian wedding and celebration market grew at 9.5% CAGR. In 2020 the market size was approximately $1020bn. Moreover, over the financial year 2022-2025, the market is likely to grow at 15% to 17% CAGR, reaching 1325-1375bn by FY2025.

Its growth will be led by the fundamental nature of the industry, high consumer spending, and the rising trend of multiday wedding functions in India.

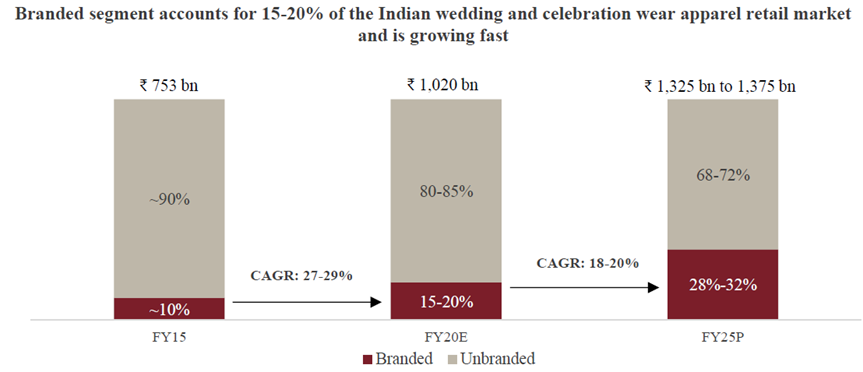

The present market share of branded clothing stores in the Indian wedding and celebration wear apparel industry is around 15% to 20%, showing enormous opportunity for branded businesses.

Between Financial Year 2020 and 2025, the branded category is expected to increase at a CAGR of 18% to 20%, accounting for 28 percent to 32 percent of the Indian wedding and celebration apparel market.

Many new players have also entered the market as Titan launched Taneira, an ethnic wear brand for sarees and ready-to-wear blouses. ABFRL bought 51 percent of Sabyasachi Couture, forged a strategic collaboration with the ‘Tarun Tahiliani’ brand by buying a 33.5 percent share, and entered the menswear market with its e-commerce brand ‘Jaypore.’

The industry initially faced a setback due to the pandemic but the demand recovered in the second half of 2021. In the future, the growth will be led by changing consumer lifestyle, raising brand awareness, and growing income levels.

In India, 9.5 to 10 million weddings take place every year, with the multiday multi event weddings in trend, rising discretionary spending and tendency to wear appropriate celebration wear, and Increased branded player penetration in tier-II and tier-III marketplaces the industry will keep on flourishing in the coming years.

3. Use of Proceeds

The issue is a complete offer for sale (OFS) where the proceeds will be paid to selling shareholders entirely after deducting relevant taxes.

- Through IPO company wishes to avail the benefits of getting listed on the stock exchange

- It expects that the listing will enhance brand visibility and image and would ensure greater liquidity for shareholders

4. Advantages

- Company with its diverse portfolio of brands is the market leader in the Indian celebration wear market, catering to the entire family.

- Increased spending on Indian wedding and celebration market

- It has a differentiated business model in terms of the mix of retailing and branded wear.

- Offer products through Omni-channel network with seamless integration of online and offline channels

- Strong Supply chain and inventory management technology-based systems in place driven by data analytics, robust processes, and strong vendor relationships

5. Risks

- The emergence of another Covid variant or any other such adversities could impact the business in the future.

- The company is majorly into a single product category- wedding and celebration wear. It is highly susceptible to the frequency and volumes of marriages and the highly-changing preferences of the customers.

- Its business is highly dependent on reputation and recognition building for its brands. Therefore, being unable to maintain its brand name could hurt its business operations.

- The company hires jobbers for manufacturing attires and accessories. Competitors can provide a better term and create a hindrance in its supply of required products.

- Most of its warehouses, factories, and jobbers are located in or around the Kolkata region, which can impact its business.

6. Financials

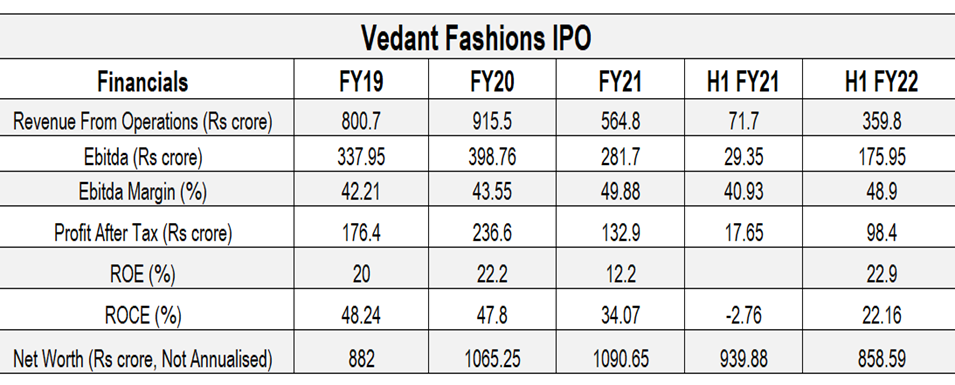

The revenue was hit by covid in the first half of FY21 while recovered in the first half of the current fiscal year. Ebitda’s margin is rising from 42.21% in FY19 to 49.88% in FY21. The numbers for return on equity have dropped from 22.2% in FY20 to 12.2% in FY21 while recovering at 22.9% in H1 FY22.

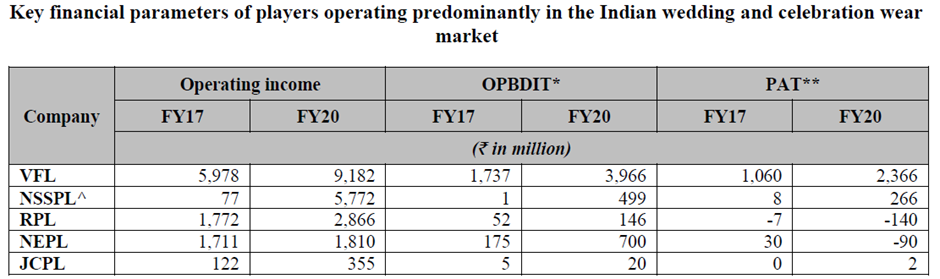

7. Peers

The data of peers operating in the Indian wedding and celebration wear market is shown in the table; vedant fashion has an operating income of Rs 9182 million in FY20, which is the highest compared to its peers. Profit after tax is positive and highest for Vedant Fashions in FY20, equivalent to Rs 2366 million, while Nalli Silk Saree Pvt Ltd (NSSPL) has PAT of 266, Ritika Pvt Ltd, and Neeru Ensembles Pvt Ltd has negative PAT numbers. VFL has shown significant growth and managed to dominate the market over the years.

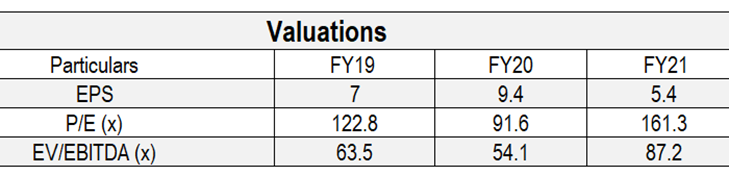

8. Valuations

The company is looking to expand its brand in existing and new geographies and even international markets. It’s Profit to earning ratio is close to 100x and 161.3x in FY20 and FY21 while P/E of 44.7x in FY24E.

One of the key takeaways from the DRHP is how the company has priced its IPO. In July 2021, the company did a buyback at Rs 495 per share and come February 2021, the company is offering the IPO at Rs 866 per share. So what really happened in the last 6-7 months that the company has priced its IPO so aggressively?

Moreover, the FY21 P/S as per the IPO price is 37x. Valuations unheard of in this industry!

9. Anchor Investors

Prior to its first public offering, Vedant Fashion collected Rs 944.76 crore from 75 anchor investors, including sovereign funds Abu Dhabi Investment Authority (ADIA) and the Government of Singapore (IPO)

SBI, Kotak, Axis, ICICI, Aditya Birla, Mirae, DSP, UTI, Sundaram, IDFC, Motilal Oswal, ITPL Invesco, Canara Robeco, and Edelweiss were among the mutual funds that together subscribed for 3.66 million shares for Rs 316.8 crore.

Other anchor investors include Fidelity Blue Chip Growth Fund, Wellington Trust, Singapore Monetary Authority, Ashoka India Opportunities Fund, Pioneer Investment Fund, PineBridge, Eastspring, Carmignac, and Colorado Venture Partners.

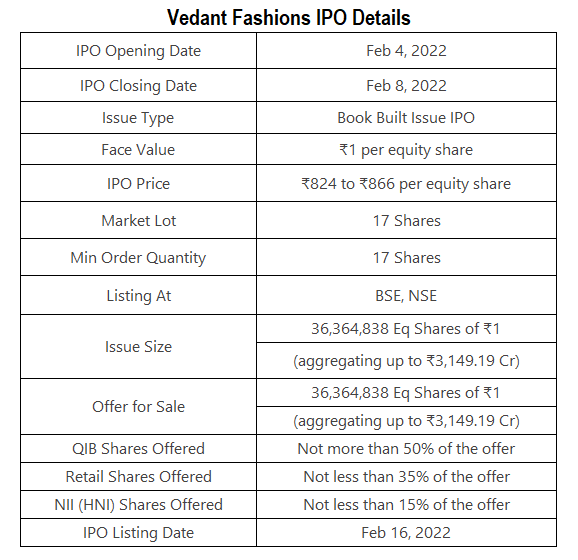

10. IPO Details

Ending Note

The Branded Indian celebration and wedding market is expected to grow at 18-20% from FY20-25; thus, the company has enormous growth potential. The company’s strategy is to expand in existing markets and enter new cities and also has a roadmap to enter new countries with an Indian diaspora.

The company has managed its revenues and operating metrics even after being hit by the pandemic in 2020. Moreover, the company has an asset-light model and a strong balance sheet with no debt. Its strength lies in its supply chain and vendor management, robust distribution models, and identifying customer preferences.

The company’s valuation and certain risk factors must also be considered. It’s essential to properly understand risks and fundamentals before purchasing the shares. While there is growth visibility for the overall industry, there is absolutely no margin of safety at the price at which its shares are being offered.

While SEBI allows such issues to be called as IPOs, this actually is an IPO-OFS (Offer For Sale). There is no fresh issue, pure stake sale by promoters.

Tavaga is everything you need to start saving for your goals, stay on track, and achieve them in time.

Download Now:

Disclaimer: Only for informational purposes. No Recommendation.