Even though markets are part of the economy, extraneous factors may buoy them

By: Tavaga Research

The curious case of the equity markets in recent months may have perplexed bystanders and active investors alike. How could the stock exchanges scale unprecedented heights when the Indian economy and its people are still in dire need of a rescue plan?

The bourses, as the purveyors of equity trading and equity shares, exchange-traded funds (ETFs), commodities, futures and contracts, and a host of related products, can work at odds with the economy. Their drivers can be different from those of a country’s economy.

The premier indices of the country, the Nifty and the Sensex hit all-time highs of 12,000 and 41,000, respectively, in the same quarter when the shrinking GDP of India (despite a recalibration by the government), hyper-inflation, an acute job crunch, consumption slump across sectors and industrial output grinding to a halt made the headlines.

Tavaga is everything you need to start saving for your goals, stay on track, and achieve them in time.

Download Now:

India’s GDP forecasted to grow at 7.5 percent in April 2019, was laboring to post even a 4.5 percent in the quarter ended September 2019.

The economic slowdown has hit the erstwhile star consumer sectors such as auto (sluggish for more than a year), FMCG, and FMCD (fast-moving consumer durables).

Core industries, powering the economy, slowed to just 1.3 percent growth in April-September of fiscal 2020, compared to 5.5 percent in the previous corresponding period. A report (by NSSO, leaked by the Business Standard) observed a 3.7 percent decline in consumer spending for the first time in 2017-18 to Rs 1,446 of individual average monthly spending.

Jobs, both hiring for replacements and new jobs, have slowed down too. Deflated sales have hampered hiring, with payroll numbers declining for the first time in November 2019, in 20 months, according to the IHS Markit India manufacturing purchasing managers’ index (PMI), a private monthly survey.

But the $2.1-trillion Indian stock market has been faring well (the dip due to the recent US-Iran tensions notwithstanding). The Sensex rose by about 3 percent in December alone, as did the Nifty. In 2019 (January to December), the Sensex gained 15 percent and the Nifty 13 percent.

Share markets work differently

Even though stock markets are a veritable part of the financial fabric of an economy, they have been known to behave independently of it at times.

Here is a lowdown of this dichotomy and what it means for the retail investor.

The foreign quotient

The stock markets are influenced by foreign investors and foreign market sentiments, just as they are by domestic investors and sentiments. Both have been at work in keeping the spirits up this time around.

Despite the US-China trade war in 2019 and the possibility of a US-Iran war clouding the horizon, indices like Dow Jones, S&P 500 (US), FTSE 250 (UK), Nikkei (Japan), DAX 30 (Germany), CAC 40 (France), and the Bovespa (Brazil) have seen double-digit percentage rise in 2019 (January-December), much like the 13-15 percent rise in the Indian indices. The dip in the first week of January 2020, seems to be momentary as US and Iran exchange threats.

International stock markets have always been correlated with each other in growth and decline.

With real-time coordination and communication, investors have the flexibility to invest anywhere in the world and reflect each other’s moods quickly.

Being a developing economy, India’s share markets have especially benefited as investments or assets here promise better returns, amid low-interest rates in the developed economies.

With the US markets soaring to record highs as well, US investors have been looking to park their bonus earnings in emerging markets.

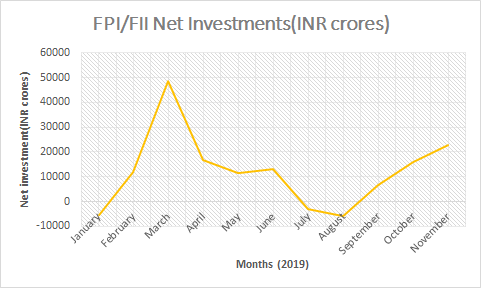

Foreign institutional investors (FIIs) known for their keen eye on finding out the most profitable option in a market, brought in net investments from September till November, after fluctuating the better half of the calendar year (decreasing net investment from March until June and net withdrawals in January, July, and August). Their vote of confidence further fuelled the benchmark rally. In November alone, the net investment of FIIs brought in around Rs 23,000 crore.

The chart below captures its net investment trend:-

Source: NSDL, Tavaga Research

Domestic equity-buying

Even when FIIs were wary (withdrawing or reducing their investments), domestic SIPs in the popular pooled investment product called mutual funds continued to grow. From April to December 2019, monthly domestic SIPs steadily ranged between Rs 8,100 and 8,500 crores. The inflow helped buoy market spirits.

The total SIP that got deposited with the MF industry between April and December 2019, increased by 8.64 percent to Rs 74,398 crore from the corresponding period of fiscal 2019.

Large-cap stocks

It may also be said that the bulk of the funds coming in via SIPs found itself directed towards large-cap, steady-performing stocks by fund managers. The rally was mostly powered by a handful of large companies (10 or so), which pulled the benchmark indices to new heights.

Companies such as Reliance Industries (RIL), ICICI Bank, and Kotak Mahindra Bank, remained mostly unaffected by the economic slowdown and gained market share profitably saw their share price appreciate.

RIL and ICICI Bank alone have ushered in half the benchmark indices’ gains. Nearly 14 of the Sensex’s 32 constituent stocks had actually registered a fall in their share price in 2019.

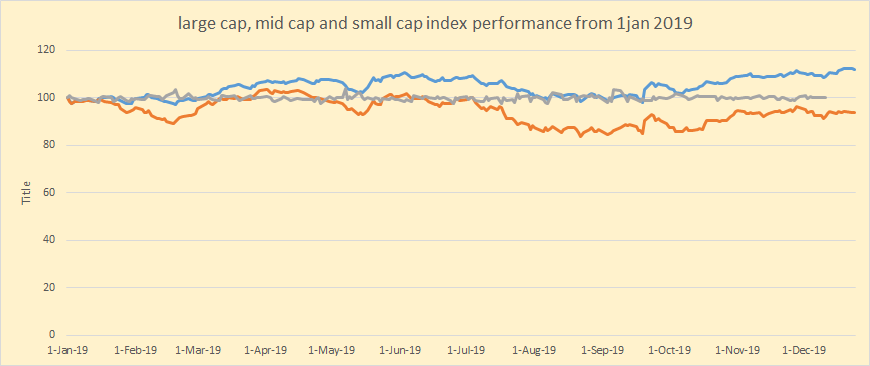

The broader market, comprising many more companies besides these, have betrayed signs of corrections. Small- and mid-caps have struggled with sluggish consumption, denting demand for their products and services.

Below is a chart showing how the Nifty 50 companies have fared well by a few degrees above mid-cap and small-cap indices on NSE in the calendar year, 2019

Source: Tavaga Research, NSE

Factoring in recovery

Of course, the popular reasoning for the stock markets’ bull run in a bearish economy is they have factored in an economic recovery.

Government moves such as cutting corporate tax rates and lowering the provisions for bad loans needed at banks saw the indices shoot up as lower corporate taxes provided a boost to large-cap stocks. Earnings, as a result, fared better in the second quarter of the financial year 2019-20 and even coaxed back FIIs as seen from their investment uptick from September onwards.

There could be a disconnect

Large-cap stocks may be holding the fort together, but recent research reports point to the high valuations in the street despite the grim economy. It could hamper gains from the stock market in the future as valuations can not increase indefinitely without accompanying profit or fresh revenue. So, the uptick could get arrested if the economic environment does not look up soon.

Not a primary indicator

The current conundrum is a reminder that we should not take growth in the stock markets as a sign of growth in the economy. Although the stock market is an indicator of the economic conditions at times, it is not a dependable one. Even though the stock markets are at an all-time high (as recently as on December 20), the GDP growth of 4.5 percent in the second quarter of fiscal 2020 has been the slowest in the last 26 quarters.

The slowdown

The doldrums the economy finds itself in is not due to a lack of stimulus. Fiscal and monetary stimuli have been announced aplenty by the government, which have got mirrored by the share markets shooting up on such news.

Structural pitfalls have led us here, according to economists, and are not letting the headline monthly indicators such as inflation, industrial production, and the overall figure of GDP growth recover.

The July-September quarter’s GDP expansion was the slowest at 4.5 percent, on the back of weakened consumer demand and the banking system chafing against a bulging bad-loan book, both results of the demonetization of 2018. Large companies in infrastructure, consumer, and capital goods are paring back their CAPEX as a result, compounding the slowdown.

Goods manufactured for exports, too, have suffered. The threat of a US-China trade faceoff and a bearish global financial climate have taken their toll. Merchandise (goods) exports in April to November of fiscal 2020 was $211.93 billion, less than $216.23 billion in the same period of fiscal 2019, decreasing by 1.99 percent. November saw a decline of 0.34 percent with exports worth $25.98 billion.

Authorities’ moves

The stock markets respond to stimulus from authorities but the economy may take time to reflect benefits if any.

To spur consumption, RBI has been slashing interest rates, including repo rate (in 2019, RBI decreased rates by a cumulative 135-bps in five consecutive cuts) but banks have been slow to pass on the cuts to the end consumers. They have even increased the risk premium in their advances, having burnt their fingers twice — with the bad NPAs (non-performing assets) and then with the NBFC-defaults (HDIL and IL&FS).

The finance ministry, too, has eased GST rates in liquidity-starved sectors like real estate and FDI norms in industrial production such as coal mining and contract manufacturing, and announced fund infusion in PSU banks, besides the corporate tax cut — all in an effort to shore up consumer demand which constitutes as much as 60 percent of the GDP.

There was a glimmer of hope when the manufacturing and services mood seemed to have improved as mapped by Markit’s PMI, which rose in November and December, from a two-year low in October.

However, the beginning of 2020 has brought news to the contrary.

FIIs have withdrawn Rs 7,505 crore from our markets in January, after a sharp decline from November’s net investment of Rs 22,999 crore to just Rs 2,762 crore in December 2019.

Most damning of all is the advance estimates of fiscal 2020’s inflation-adjusted GDP growth, which has been pegged at 5 percent, marking the year as the third straight one to witness a slowdown and the lowest in growth in six years. Applied for the Union Budget planning of the next year, the advance estimate could call for more austere measures.

The government is struggling with a revenue shortfall (meaning lower than projected tax collections) of around Rs 2.5 lakh crore.

Observers were anticipating a sharp cut in government spending, as a result, for the remaining three months of this fiscal, by as much as Rs 2 lakh-crore (that’s around $28 billion).

A government’s spending is one of the key tools to spur an economy during a slowdown, especially when private-sector spending is dismal. Till November, ours have already spent 65 percent of the budgeted Rs 27.86 lakh crore.

But it seems, according to reports, the government will be making an extraordinary demand of RBI to pay it another interim dividend of anywhere between Rs 35,000-45,000 crore. It will be the third consecutive year for such a handout to the Union government, and just months after the previous RBI sanction of Rs 1.76 trillion in a dividend payout (including Rs 1.48 trillion for fiscal 2020).

We may have to batten down the hatches in these times of financial crisis, with simple steps like being a bit more judicious with our spending.

It is unlikely the sluggishness will give way to a full-blown economic recession given India’s undeniable organic growth momentum, but it may take longer to recover than what our stock markets would have us believe.

Retail investors should refrain from getting swayed by the mercurial benchmark movements and focus, instead, on the earnings of the companies and their future prospects. In other words, these are the times when even the wisest among us may think it is easy to time the market. Or, suffer a lingering regret of not profiting from the rally.

It is best to not review our portfolios at such times and stay the course. Changing our investments or choosing a new path may be tricky. Rather than focusing on the returns, we could look at the risk profile of our goal-based strategies of investment at this time, and see if we are protected from such dual trends in the world of finance.

The performance difference between the benchmark indices and the broader markets is quite high right now. Hence, trying to cash in on news on the economy recovering could be riskier than focusing on long-term investments with the potential to perform well and earn us returns.