Total Amount Invested

Total Wealth Generated

SIP-ping liberates us from the need to be antsy about market’s ups and downs, and our calculator helps further

The slump in the economy and its impact on the downcast equity markets have made staid investors rethink about staying invested.

But amidst the gloom and doom, knowing a little more about the popular investing route of systematic investment plans (SIPs) could shed some light on why they still make sense.

SIPs are often the method the average retail investor takes to invest in equities. SIPs are not synonyms for mutual funds (MFs) but are a way of investing in them.

Infact, SIPs can be a strategy for investing in other baskets or funds comprising numerous securities such as ETFs. SIPs in single stocks are also a possibility, though that would require us to be more mindful of the workings of the market. Debt funds, in both MFs and ETFs, can also be subscribed through SIPs.

We can start with as little as Rs 500 a month with an SIP. The Association of Mutual Funds (Amfi) puts the average SIP size at about Rs 3,000 an account, with 954,000 accounts opened each month in the current financial year (FY2019-20).

In investor parlance, timing the market means buying ourselves assets when the market is at its lowest, and essentially avoiding shelling out more money when the prices are at their highest. This ensures we spend less but gain the most when there is an uptick in value. However, with a timing-ignorant but consistent approach we won't be worse off.

For an SIP investor, there should be no reason to panic unlike those brandishing a lump sum amount. With SIPs, we are investing in increments and at regular intervals.

The installments buy us units of our chosen scheme at different prices (the unit price is called Net Asset Value or Nav). Higher price would mean we buy less units with that installment and low prices gets us more units.

With cyclical ups and downs, over time, the good (low price) averages the bad (high price) out and leaves our investment corpus to reap the benefits of returns on the fund. There is, of course, a name for it -- rupee cost averaging.

The returns may vary depending upon the stock market performance and the SIP calculator also doesn’t take into consideration the exit load, commission, expense ratio, and other charges, if any.

SIP Formula:

Maturity Amount or FV = P × ({[1 + R]n – 1} / R) × (1 + R)

Where,

FV = Future Value

P = Periodic investment amount

R = Expected return

N = Number of periodic payments

As a result, our average investment cost remains reasonable for those of us who don't want to get into the cryptic practice of timing the market. With small amounts spent at regular intervals, there would be times when we will catch the lowest price of the fund, the best scenario, and this will balance out the times we will end up paying the highest price on the fund.

A one-off lump sum investment won't afford us the boon of rupee cost averaging. Of course, we have to consider a sizeable period of at least five years to start benefiting from it with an SIP.

Source: Tavaga Research

Source: Tavaga Research

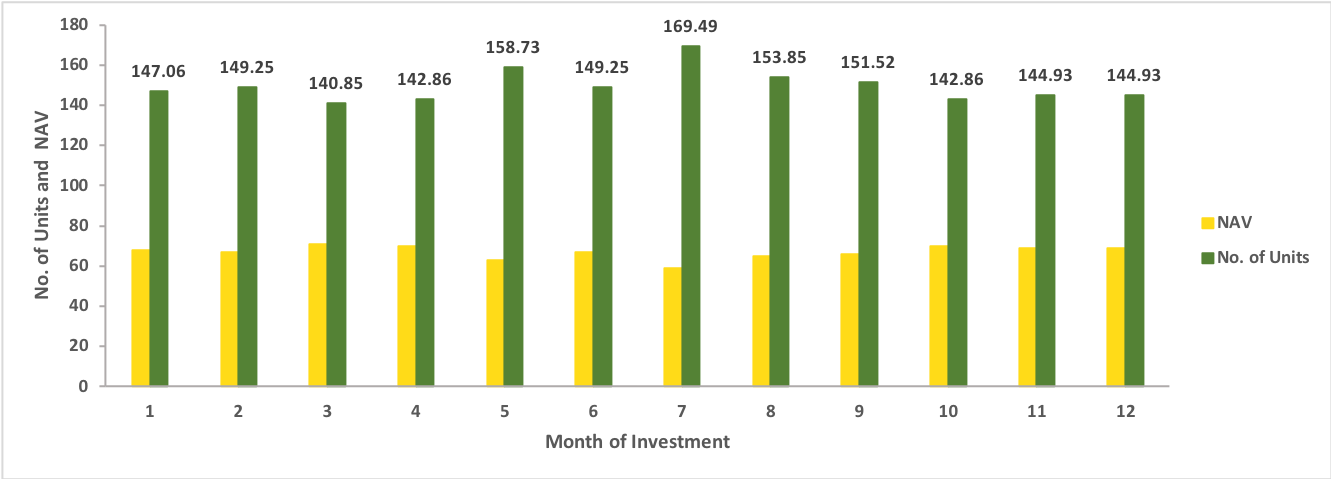

The above is an illustrative chart on how rupee cost averaging works for us, the investors -- buying different units at different prices over a year. It evens out the blows from high unit prices by getting us more units when the price is low.

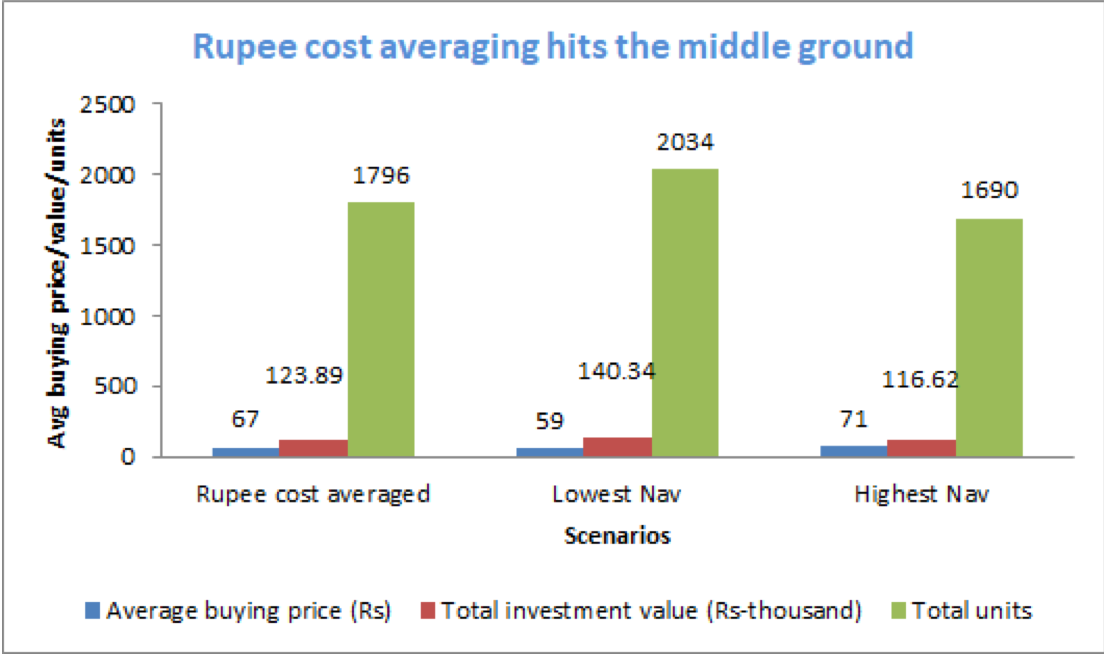

Using SIPs, we can hit the middle ground, on both total units and value of investment, between a bad and a good market, as the following chart captures:-

Source: Tavaga Research

Source: Tavaga Research

In the present volatility, as the indices head south, withdrawing from the markets or stopping an SIP defeats the purpose. A move akin to timing the market, it gives in to undue panic and overlooks the benefit of rupee cost averaging.

Data sourced from Passivefunds.in shows, over a period of 282 months, from 1995 to 2019, the portfolio which did not time market to not have done too badly, driving home the fact that we don’t have to fret over when to invest.

SIPs are also mighty good at instilling discipline, a trait every investor should hone. The auto-debit of an SIP hides away a part of our money from us at regular intervals. Now, any investor with an iota of self-discipline will tell us why that is such a good idea. This serve as a reminder that hiding money from ourselves is a winning way to discipline even the most errant investor.

By removing the need for triggers to invest, be it for that elusive ‘right time’ or for a windfall lump sum, SIPs nudge us towards putting our earnings away from our spending selves, and in places where they work to earn more.

Everything from the current cost of each of our financial goals, years till their achievement, an estimate of average inflation, and the expected rate of return on the instrument we choose for an SIP should go towards informing the amount we pay. Of course, an SIP calculator helps to make the task easier for us.

However, we will have to be mindful of the bank’s charges on a failed auto-debit in its ECS (electronic clearance service).

But if we miss our SIP payments for three consecutive turns, then the fund houses usually cancel our SIP and stop debiting our account for investment. We would have to reapply to get back in.

Standing instructions - If we are juggling between more than once account, especially one for SIP and another for salary, standing instructions could help an auto-debit from the source of funds to the investment account.

There are options to buy fund units ad hoc online or through offline channels. A missed SIP purchase could be compensated by opting to manually buy units.

We could also avail of the facility with some funds to invest a lump sum with an ongoing SIP.

But then again, the point of an SIP is to not having to get antsy about our equities or money market investment but be secure in its regularity. So, acting on missed SIP should ideally be about promising ourselves not to miss one again.

There might be times when we would still want to cancel our SIP. We could be relocating abroad, want to invest somewhere else instead or simply want to change funds to invest in.

Cancelling an SIP requires us to inform the AMC or our agent. It can be done online or through offline forms with details of the folio number, SIP account, bank account, SIP amount etc. Cancellation might take a month to process.

In tandem, we will need to inform our bank to stop the ECS or auto-debit, as it will stop payments even if there is a delay in processing at the AMC’s.

We can also temporarily stop payment if the need arises by instructing our bank to stall auto-debit. But again, after three missed SIPs, the fund house will cancel our arrangement.

Some fund houses let us pause the SIP withdrawal but it is for a limited period of time and can be done only once in our SIP tenure.

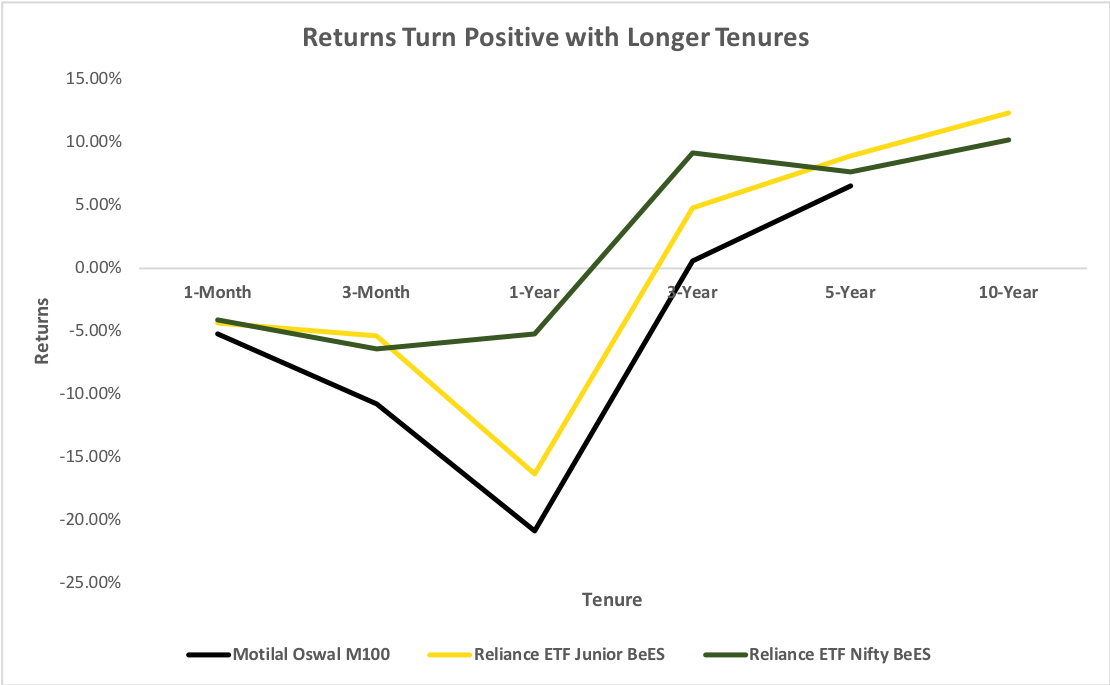

But if we stay invested for more than six years, ideally even 10-15 years, we increase the probability of catching the improvement in market sentiments and earning good returns to compensate for any intervening slumps in the market.

This chart shows how ETF returns increase considerably with time, across funds:-

Source: Tavaga Research

Source: Tavaga Research

Top-up SIP: This is an option which can arm us better to fight inflation. We can increase our SIP amount yearly with a top-up SIP, as our income increases.

Flexible SIP: This option allows us to increase or decrease the SIP amount with predetermined market conditions, say the unit price changing by a specific percentage or a particular market valuation.

Perpetual SIP: If we do not mention an end date in our SIP mandate when signing up to denote a fixed tenure, it is considered as a perpetual SIP. It leaves the decision for when we want to redeem for later, if we feel our financial goals are fluid and need more time.

For all the reasons we have mentioned so far, SIPs accumulate wealth in a more reassuring manner than one-time investments.

We might dread not being able to buy more units when the market prices rise with an SIP but that is a misplaced fear. A lump sum higher than our SIP might buy us more units at that time, but as a sustained strategy, it is more volatile for the average investor.

Comparisons between lump sum and SIP for just a year’s worth of investment might yield a result favouring the former. It goes on to show with an SIP, we will be better off looking at a sustained, long-term plan of 10-15 years. Lump sums can work for the savvy in the short term.

So, we can put our lump sum in our SIP bank account and let the auto-debits do their work, staggering our entry at different unit prices.

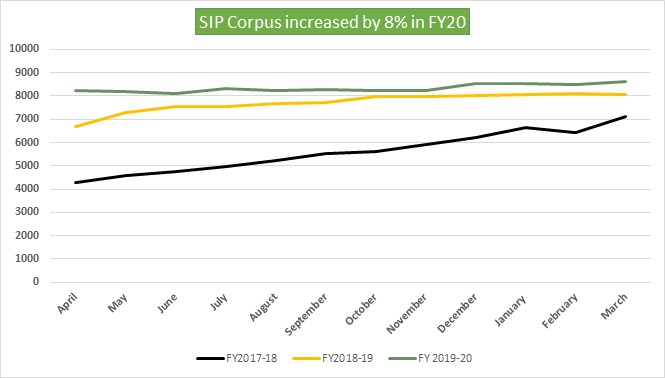

Amfi reckons there are currently 33.1 million SIP accounts (as of August 2020), opened by investors. The SIP contributions have only increased in leaps and bounds over the past few years as shown in the chart:-

Source: Tavaga Research, AMFI

Source: Tavaga Research, AMFI

At the end of it all, investing well hinges on being able to make the most of the compounding effect. Returns on our investments become a part of that very investment, as we stay invested, and earn us further returns.

With an SIP, we will be comfortably on our way to enjoy the fruits of compounding.

Treating SIP as a savings tool just as much as it is an investment route can prove to be a useful reminder if we ever think of discontinuing.

Many of us, including those at the start of our careers, earn enough to invest. But we just don't save enough to do so. SIPs help us save and invest, a twin bonanza.

for India

for India